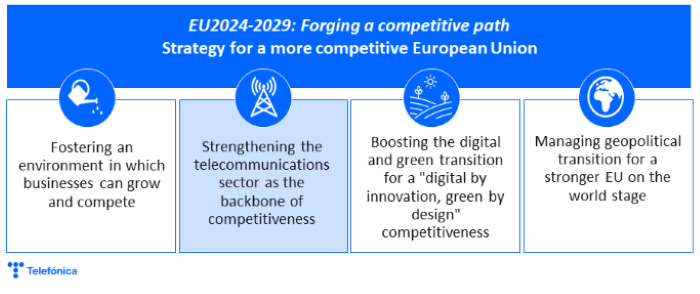

In June, we launched the series EU 2024-2029: Forging a competitive path to share Telefónica’s vision on how to strengthen competitiveness and better position the European Union (EU) society and economy on the global stage. Strengthening competitiveness is undoubtedly the European strategic priority for the 2024-2029 cycle in the face of slowing economic growth in the EU.

If the first post analysed the current state of EU competitiveness, the second one focused on the first axis of the competitiveness strategy proposed by Telefónica: the creation of a regulatory environment that allows European companies to grow and compete. In this third post we focus on the second strategic axis: the importance of strengthening the telecommunications sector as a lever for competitiveness in society.

The telecommunications sector is the backbone of competitiveness

Strengthening the competitiveness of European companies means increasing their productivity. Productivity growth is influenced by a number of factors such as innovation, efficiency gains and technology diffusion.

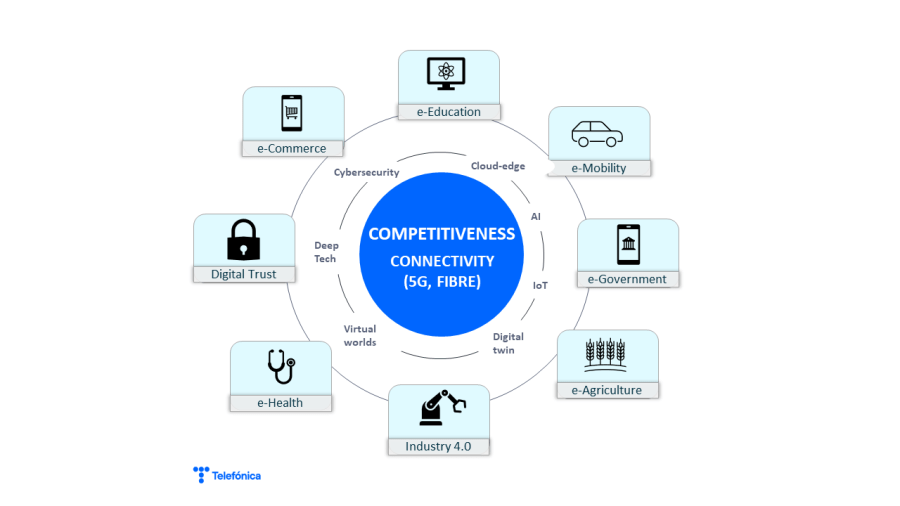

In all cases, the telecommunications sector plays a key role. Telecommunications companies are at the forefront of the development and transformation of the digital infrastructure and services that underpin the digital economy and society. Economic and social progress depends on the availability of high-capacity fixed and mobile networks. Similarly, it would not be possible to strengthen the EU’s digital leadership, which is crucial for maintaining the region’s international relevance in an era characterised by digitalisation and new technologies.

Over the past decade, the telecommunications sector has invested an average of EUR 50 billion per year in order to modernise and adapt network capabilities to anticipate and meet the growing demand for broadband-intensive digital services. It has also facilitated the development of enhanced products and services, as well as the creation of new avenues for technological innovation across a range of economic sectors.

The next wave of digital innovation, based on technologies such as 5G, IoT, edge-cloud computing, and artificial intelligence (AI), will lead to the creation of new applications and economic opportunities. To realise their full potential, it is crucial to invest in these technologies, to enhance network capabilities and to evolve towards programmable networks through the use of standardised APIs (Open Gateway).

This evidence shows that the telecoms sector is characterised by a constant process of increasing efficiency, innovation and adaptation. The sector’s collaboration in the diffusion of technology to other sectors is of great importance, given the sector’s reach and technological sophistication.

Market Structure: the challenge for the EU telecoms sector

The competitive landscape has undergone significant shifts in the past 25 years, following the advent of liberalisation. The sector is currently facing competition from players in adjacent markets, as well as from international platforms offering low-cost or free services in a two-sided business model.

For the sector to remain competitive, it is essential that the market structure is able to adapt effectively in a dynamic way, without the introduction of artificial policies that could distort the market. This is crucial because fair and sustainable competition stimulates innovation and investment, which in turn improves the quality of services provided to society and its citizens.

In this context, higher market concentration in terms of number of competitors does not mean less competition. Indeed, in certain markets, such as telecommunications, increased concentration has led to more efficient firms gaining market share, while less competitive ones have exited the market. In other words, market concentration would be a consequence of restructuring a competitive market towards efficient and sustainable market structures.

In his report, Enrico Letta emphasises the need to increase the scale of the telecommunications sector in the markets where its networks are deployed. In this sector, the lack of scale is determined by the high degree of fragmentation within each national market, which makes it difficult for them to achieve the necessary level of market take up to be viable. This fragmentation is fostered by a regulatory and price competition approach that encourages the creation of new artificial competition, through regulatory privileges.

Today, in a European market with more than 100 operators, keeping the focus only on pro-entrant regulation, would be detrimental for a technology switch towards advanced networks that require massive investments

Sector viability and connectivity goals at risk

The regulatory and competition policy approach that was used to liberalise the sector at the end of the 20th century is no longer fit for purpose in today’s markets.

On the contrary, this approach is hampering the viability of the sector and its ability to invest at a crucial time, when the EU must stimulate investment to meet the 2030 Digital Decade connectivity goals, for which an investment deficit exceeding €200 billion is estimated.

We are far from the targets as the data show, and this has an impact on the welfare of European citizens, who must in any case be defined as more than mere consumers.

Public policies for a telecommunications sector as the backbone of competitiveness

European public policies should encourage investment in ultra-broadband networks. This should create incentives for investment, innovation and job creation, and reduce barriers to the deployment of connectivity infrastructures. It is therefore recommended to:

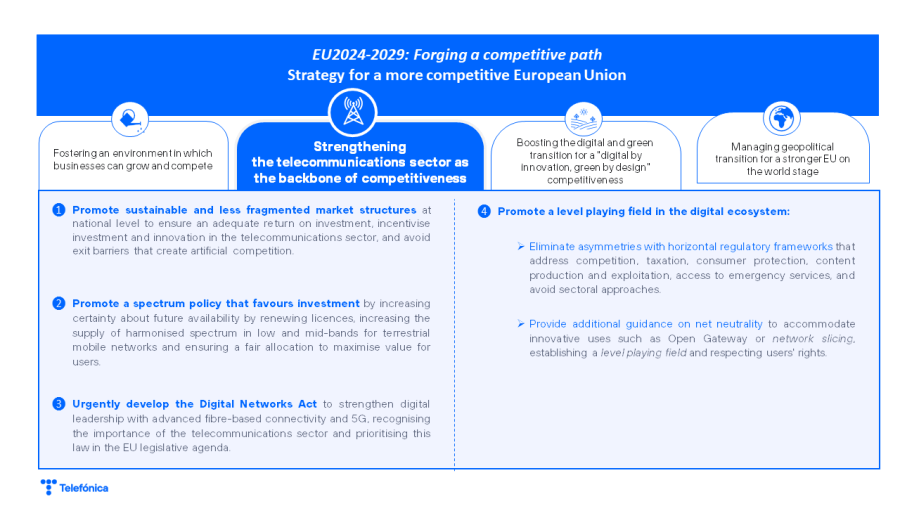

- Promote sustainable and less fragmented market structures at national level to ensure an adequate return on investment, to encourage investment and innovation in the telecoms sector, and to avoid exit barriers that create artificial competition.

- Promote an investment-friendly spectrum policy by increasing certainty about future spectrum availability through licence renewal, increasing the supply of harmonised spectrum in the low and mid-band for terrestrial mobile networks and ensuring a fair allocation to maximise value for users.

- Urgently develop the Digital Networks Act (DNA) to strengthen digital leadership with advanced fibre-based connectivity and 5G, recognising the importance of the telecoms sector and prioritising this Act in the EU legislative agenda.

- Promote a level playing field in the digital ecosystem:

- Eliminate asymmetries with horizontal regulatory frameworks that address competition, taxation, consumer protection, content production and use, access to emergency services, and avoid sectoral approaches.

- Provide additional guidance on net neutrality to allow for innovative uses such as Open Gateway or network slicing, creating a level playing field and respecting users’ rights.

In the next posts we will delve deeper into the next strategic axis for a more competitive EU: how to boost a competitiveness “digital by innovation, green by design“.