Industrial policy is in the spotlight. Two forthcoming reports will shape the future of European policy. Enrico Letta, President of the Jacques Delors Institute, will deliver his report on the future of the single market in March, and Mario Draghi will present his recommendations for restoring competitiveness after the European elections in June.

For the third consecutive year, ETNO publishes the State of Digital Communications 2024, a report that analyses the competitiveness of the European digital sector compared to other regions such as the United States, Japan, South Korea or China, based on over 70 KPIs.

In a context where innovative connectivity is increasingly critical to competitiveness and economic security, where does Europe stand?

Network innovation is starting to take off

The 2024 edition presents a broader perspective than its predecessors, keeping track of network innovation through the analysis of 5G SA (standalone) deployment, RAN technologies and edge-cloud dynamics. This years’ report concludes that network innovation is starting to take off in Europe.

Looking at 5G SA and RAN technologies, of the 114 operational 5G networks in Europe, only 10 included 5G SA and 11 had RAN technology developments. Regarding edge-cloud which remains at the heart of network virtualization, Europe lags behind both Asia and North America, with only 4 edge-cloud commercialised offers compared to Asia’s 17 and North America’s 9.

The financial health of the European telecommunications sector needs to be strengthened

According to ETNO, European telecom operators have invested over €59 billion in 2022 (from €56.3 billion in 2021). Around 48% of the investment was oriented to fixed access, over 20% to mobile access, and the rest covered aggregation and core transport networks, IT and various non-network assets such as offices. In comparison, content and application providers (CAPs) in Europe spent €17 billion on digital infrastructure, of which 94% on data centres.

Although telecoms sector high investments and progress in network innovation, the sector’s financial situation needs to be reinforced to strengthen Europe’s strategic autonomy. While other regions are seeing the value of the telecom sector and its operators grow, the European sector continues losing size.

European telecom operators’ revenues have been declining in real terms

European telecom operators have been absorbing inflation on behalf of their customers, with real telecom revenues declining steadily since 2016 and falling sharply in 2022 (-7.1% below the evolution of the consumer price index).

Average revenue per user (ARPU) continues to lag behind other peer regions. For example, in the United States, mobile ARPU is almost three times higher than in Europe in 2022 (€15 in Europe compared to €42.5 in the US). This difference is also evident in fixed broadband, where the average revenue per user in Europe is €22.8, compared to €58.6 in the US.

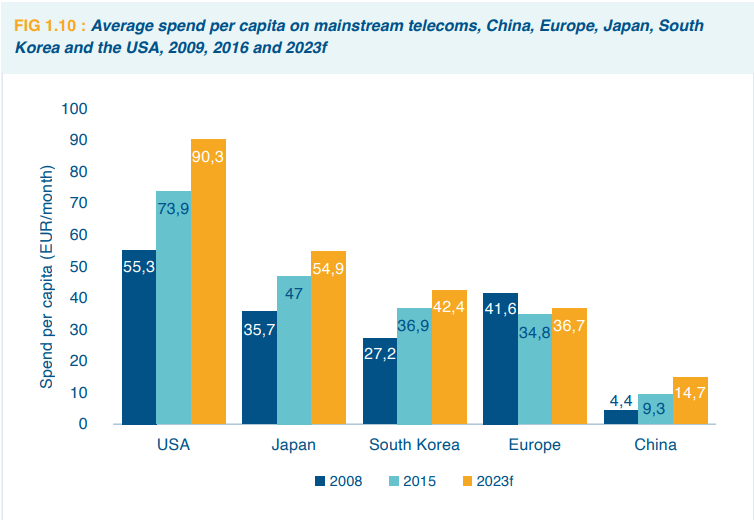

According to ETNO, in general, Europe continues to register lower monthly per capita spending on telecoms (€36.7) in comparison to Japan (€54.9), South Korea (€42.4) and the USA (€90.3), and unlike these regions, the trend has been downward since 2008.

Lower revenues and returns translate into lower investment capacity

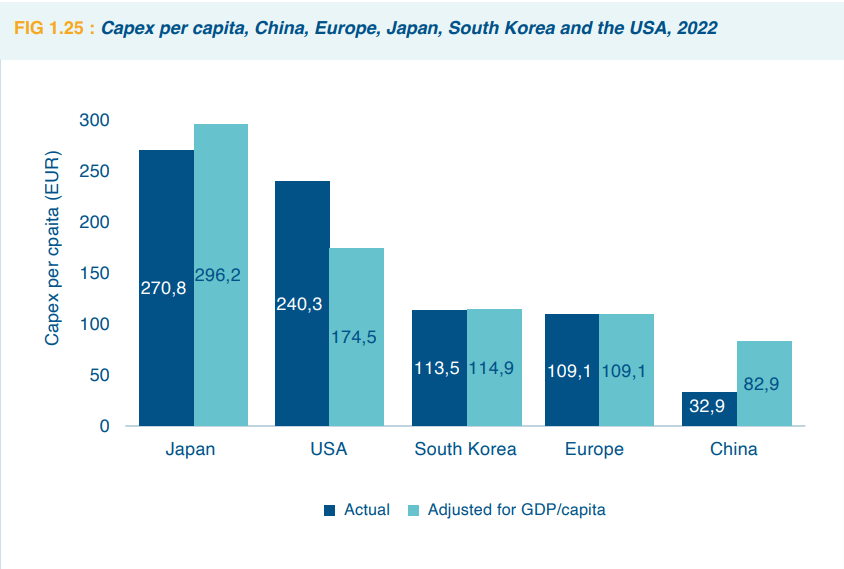

Lower revenues have resulted in operators with lower investment capacity compared to operators in other regions. In terms of investment per capita, Europe (€109) lags behind Japan (€270), the US (€240) and South Korea (€113). This investment gap shows no signs of narrowing.

In 2022, the capital intensity of European telecoms companies, as measured by capex relative to revenues, remains high at around 20%, above its peers. This, combined with declining revenues, is leading the sector to higher debt levels, which, according to ETNO, are at 2.60 times net debt to EBITDA. This highlights the financial pressure the sector is under and the need to manage investments and debt in the coming years.

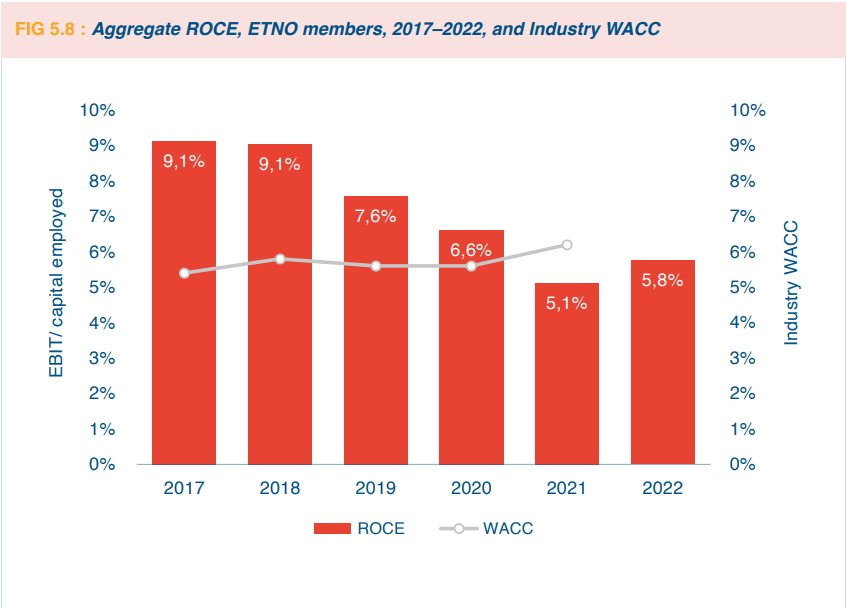

Lower rate of return of the telecommunications industry in Europe

ETNO points out as a cause of this financial stress that European retail markets remain uniquely fragmented. In 2023, Europe counted 45 large mobile operating groups with more than 500.000 customers, compared with 8 in the USA, 4 in both China and Japan, and 3 in South Korea.

The lower rate of return of the telecommunications industry (5.8%), as a consequence of the regulatory and competitive landscape in Europe is incompatible with the vision of open strategic autonomy and the long-term sustainability of investment efforts in Europe.

Gigabit-capable coverage and share of 5G usage progresses more slowly in Europe

This situation is impacting in the rollout of quality connectivity based on gigabit and 5G networks, which is progressing more slowly in Europe.

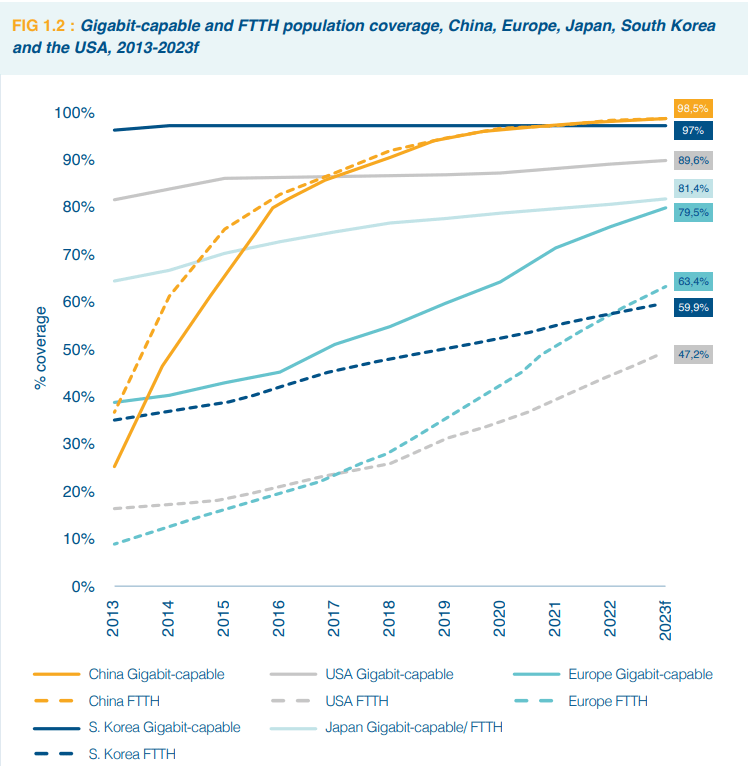

Gigabit-capable access networks cover 79.4% of Europeans. The goal is to reach full coverage in 2030, however Europe remains behind its regional peers (e.g., US covers 89.6% of its population).

4G mobile networks in Europe cover more than 99.8% of the population. But only 80% of the European population is currently covered by 5G networks. Europe’s coverage is still far from its digital goal for 2030 (100% coverage) and is lower than all peers: China (89%), Japan (94%), South Korea (98%) and the US (98%).

As a result, average European mobile downlink speeds (64 Mbps in mobile and 121 Mbps in fixed networks), although higher than the global average, are significantly lower than those in other regions, such as the US (97 Mbps in mobile; 214 Mbps in fixed networks)

Finally, 5G share of mobile connections has grown significantly in Europe recently but is dramatically lower than in other regions (17% in Europe vs 83% in China or 49% in the US in June 2023).

Lead or lose moment for Europe’s connectivity ecosystem

This calls into question Europe’s ability to meet the objectives of the European Digital Strategy 2030 and drive the region’s leadership in the technologies of the future. It also emphasizes the need to take action to revert the trend.

To play its rightful role and secure its place in the world, Europe must put its economy back on the road to competitiveness. It must regain leadership and ambition in the connectivity space: get the scale right, simplify frameworks and obligations, trust business to lead change, and in short, rethink its approach to consumer, competition policy and regulatory model, while levelling the playing field for a fair share and efficient use of networks.