Madrid, 5th November 2019

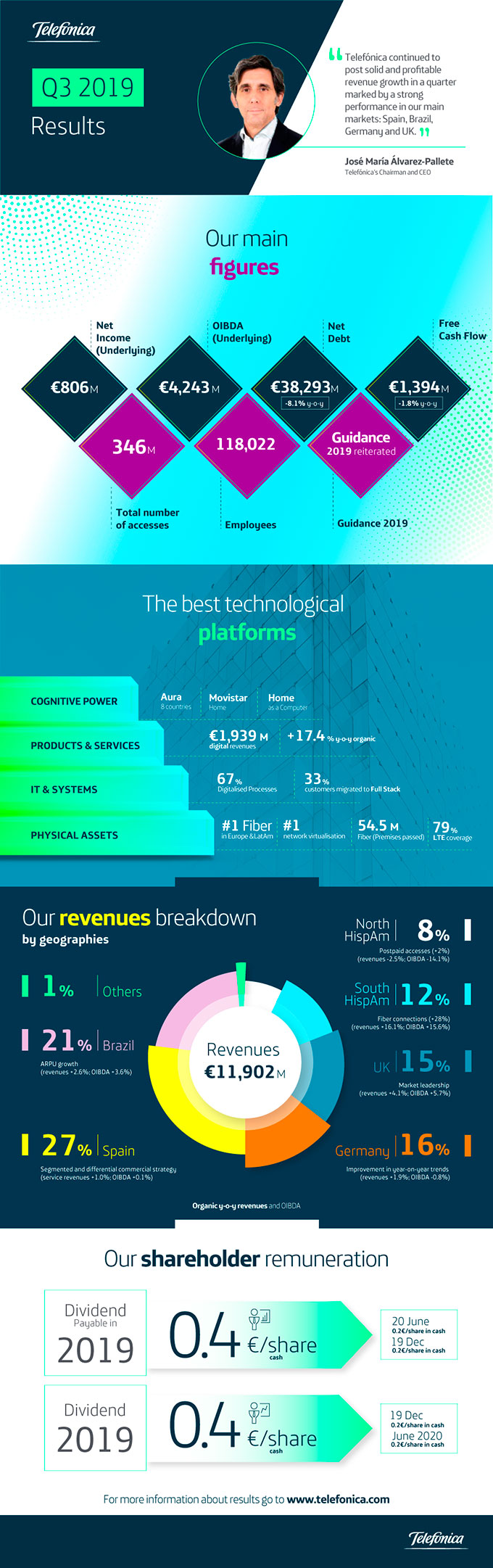

Net income reached €2,588M excluding extraordinary items, mainly restructuring expenses in Spain

Highlights:

- Telefónica boosts revenue growth (+1.7% reported) compared to 3Q18, thanks to the improvement in Spain, Brazil and Germany, to the strong performance of the United Kingdom, and despite the negative impact of currencies. In organic terms, revenues grew 3.4%. Average revenue per user (ARPU) also increased in the quarter (+4.3% year-on-year organic) and churn rate improved.

- Solid performance in main markets: Spain accelerated organic revenue growth in the quarter (+1%) thanks to the progress of the customer, businesses and wholesale segments, while Brazil achieved the highest revenue growth in the last 15 quarters (+2.6%). In addition, revenues grew 1.9% in Germany thanks to the good commercial momentum, and the United Kingdom reiterated its leading position in the market, with a clear improvement in accesses (6%) and sales (+4.1 %). This helped offset the drop in revenues in Hispam Norte, affected by competitive intensity.

- Strong growth in digital revenues, +17.4% year-on-year in the July-September period, to a total of €1,939M.

- Extraordinary items in the quarter: The third quarter of 2019 recorded €1,876M of provisions for restructuring expenses, mainly in Spain (€-1,732M). These provisions, part of the process of transformation and simplification of the company, have not affected cash generation.

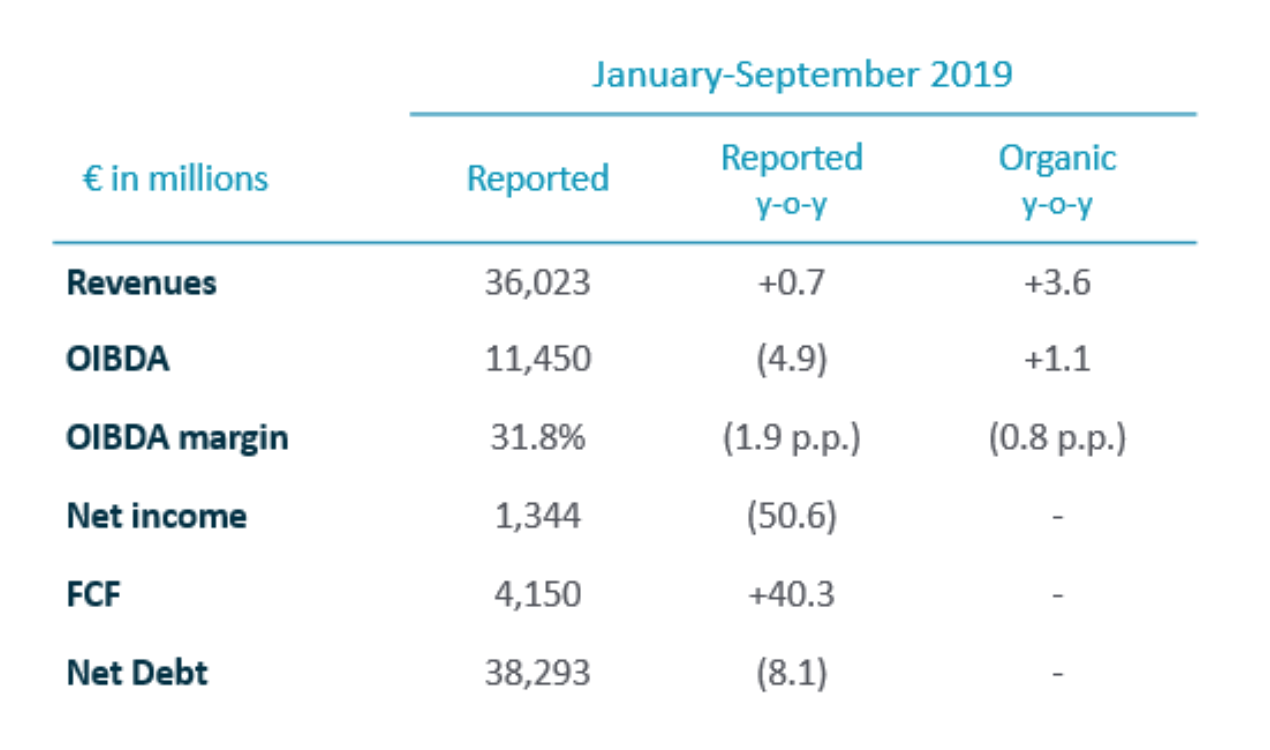

- Debt reduction for the 10th consecutive quarter.. Net debt stood at €38,293M (-8.1% year-on-year), thanks to a 40.3% increase in free cash flow and reached €4,150M in the January-September period. Including post-closing events, debt would be approximately €37.6 billion.

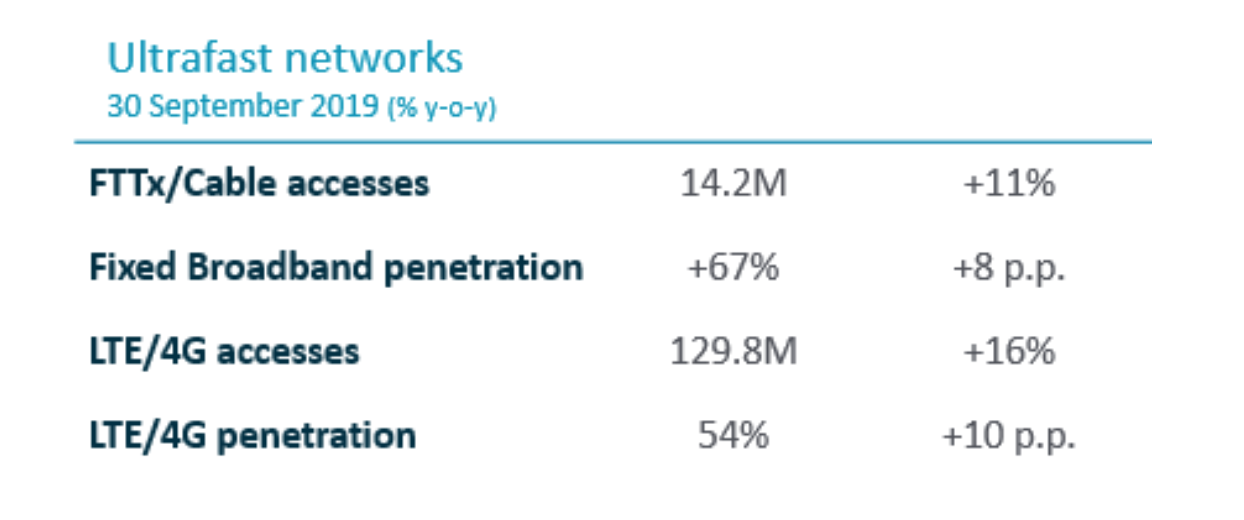

- The company continued to deploy ultrafast networks: Telefónica’s fiber reached 123 million premises passed, of which 54.5M (+11%) pass through its own network. 4G coverage is close to 80%.

José María Álvarez-Pallete, Chairman and Chief Executive Officer:

“Telefónica continued to post solid & profitable revenue growth in a quarter marked by a strong performance in our main markets, Spain, Brazil, Germany and UK. We continued to generate very strong free cash flow, up 40% year-on-year in the first nine months of 2019, driving a reduction in net debt for the 10th consecutive quarter.

We made good progress on key strategic initiatives to simplify our business this quarter, including a workforce restructuring program in Spain. We are forging ahead with plans to monetise further our mobile telco infrastructure, making a more efficient use of our networks by sharing them, whilst adding new partners to enrich the value of our commercial offer in the home.

Telefónica remained focus on deploying next generation networks in our markets, improving our 4G coverage and launching 5G selectively, as we have in the UK. Looking ahead, we reiterate our guidance for this year and are confident that our digital transformation will boost returns and deliver the best technological solutions for our customers.”

Financial results January-September 2019:

Telefónica today presented its results for the January-September period, which stand out for the return to reported growth in revenues in the third quarter, thanks to the improvement in Spain, Brazil and Germany, and the strong performance of the United Kingdom, despite of the negative impact of currencies. Telefónica advanced in the deployment of ultrafast networks and reduced net debt for the tenth consecutive quarter. The company reiterates all the objectives set for the year, as well as the dividend corresponding to 2019.

Focus on high customer value

Telefónica Group’s access base stood at 345.8m at September 2019, virtually stable y-o-y excluding changes in the perimeter. The continued quality improvement of the customer base explained the growth in average revenue per access (+4.3% y-o-y organic; +4.7% in January-September), while churn improved 0.2 p.p. both y-o-y and q-o-q.

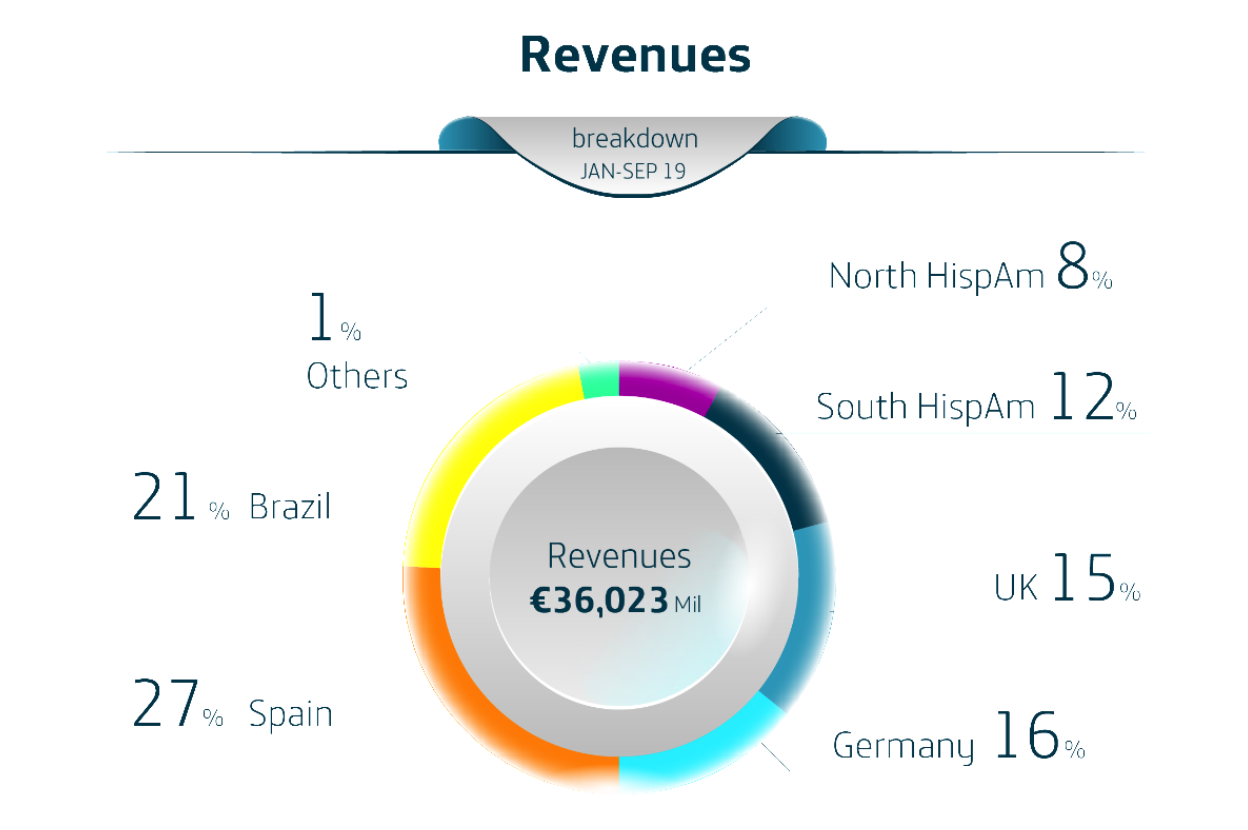

Revenues totalled €11,902m in the third quarter (€36,023m in January-September) and increased by 1.7% y-o-y (+0.7% in January-September). In organic terms, revenues increased by 3.4% y-o-y in the third quarter (+3.6% in the first nine months), reflecting an acceleration in handset sales growth (+17.0%) and sustained service revenue growth (+1.8%).

Revenues coming from broadband connectivity and services beyond connectivity accounted for 55% of the total (+2 p.p. y-o-y), reflecting the transformation of the revenue mix and increasing business sustainability, while voice and access decreased by 3 p.p. to represent less than a third of the total.

In the third quarter, provisions for restructuring costs amounted to €1,876m (€34m in the same period of 2018), mainly in Spain (-€1,732M). These provisions did not impact free cash flow generation in the quarter and were carried out within the company’s transformation and simplification process, which shall enable the generation of incremental savings and efficiencies with a positive impact on cash generation.

Exchange rates negatively affected the Company’s reported results for January-September 2019, mainly due to the depreciation of the Brazilian real and the Argentine peso against the Euro. In the third quarter, foreign currencies reduced y-o-y revenue growth by 2.0 p.p. and OIBDA by 1.5 p.p. mainly due to the evolution of the Argentine Peso, though the trend improved sequentially on better y-o-y comparison of the Brazilian real against the Euro (-3.7 p.p. and -3.2 p.p. respectively in the first nine months).

Operating income before depreciation and amortisation (OIBDA) reached €2,748m in July-September (€11,450m in January-September), affected by the above-mentioned factors. In organic terms, OIBDA grew by +0.8% y-o-y in the quarter (+1.1% in the first nine months). OIBDA margin stood at 23.1% in the third quarter (-11.4 p.p. y-o-y; -0.8 p.p. organic), mainly affected by the provision for restructuring costs. In January-September, OIBDA margin reached 31.8% (-1.9 p.p. y-o-y; -0.8 p.p. in organic terms).

Net income (-€443m in July-September; €1,344m in January-September) was mainly affected by the provision for restructuring costs of the third quarter. However, net income reached €806m in July-September, after excluding restructuring costs (-€1,402m), capital gains (+€267m) and other factors (-€114m). For January-September, underlying net income was €2,588m.

CapEx: (+ 17.2%) excellent connectivity, quality and customer experience

CapEx in January-September was €6,657m (+17.2% y-o-y) and included €1,465m of spectrum (€1,443m in the third quarter of which €1,425m in T. Deutschland, with no impact on free cash flow in the period following the approval of a deferred payment schedule). Capex continued to focus on accelerating excellent connectivity, deployment of LTE and fibre networks, increased network capacity and virtualisation and improving quality and customer experience (implementation of AI in the Company’s technology platforms).

Net financial debt at September 2019 (€38,293m) decreased by €2,781m vs. December 2018 thanks to free cash flow generation (€4,150m), net financial divestments (€1,170m; sale of 9 Data Centers, T. Panamá, T. Nicaragua, T. Guatemala and Antares) and the issuance and replacement of capital instruments (€686m). In the third quarter, net financial debt decreased by €1,937m thanks to free cash flow generation (€1,394m), net financial divestments (€849m; sale of 9 Data Centers and T. Panamá) and the issuance of capital instruments (€500m).

In January-September 2019, the financing activity of Telefónica amounted to €6,899m equivalent (without considering the refinancing of commercial paper and short-term bank loans) and focused on maintaining a solid liquidity position and refinancing and extending debt maturities (in an environment of low interest rates). As of the end of September, the Group has covered debt maturities for the next two years. The average debt life stood at 10.7 years (vs. 9.0 years in December 2018).

Digital transition: sustainable and profitable growth

Telefónica made progress in the digital transition towards sustainable and profitable growth, upgrading its network infrastructures and providing excellent connectivity in speed, coverage and security. The Group’s fibre and cable (FTTx/cable) network reached 123m of premises passed (54.5m own network; +11% y-o-y) and LTE coverage already reached 79% (+2.3 p.p. y-o-y; 95% in Europe and 73% in Latin America). Fiber investment is key for Telefonica and will allow revenues generation and efficiencies by capturing savings thanks to copper networks shutdown plans.

The Group achieved 80% of the 2019 savings targets (>€340m on top of >€300m achieved in 2018) in the first nine months of the year, thanks to the E2E Digital Transformation programme. The main drivers for the transformation were the improved digital experience in sales process, the digitalisation of customer services and the process automation.

Revenues in the business segment rose 3.7% to €2,263m y-o-y in the quarter (Europe: €1,270m, +1.3% and Latin America: €993m, +6.5%). Digital services continued to drive B2B revenue growth (+28% y-o-y), primarily Cloud, IoT and Security.

Digital services revenues reached €1,939m in July-September (+17.4% y-o-y) and €5,722m in the first nine months (+19.2% y-o-y).

Results by geographies:

(% organic y-o-y)

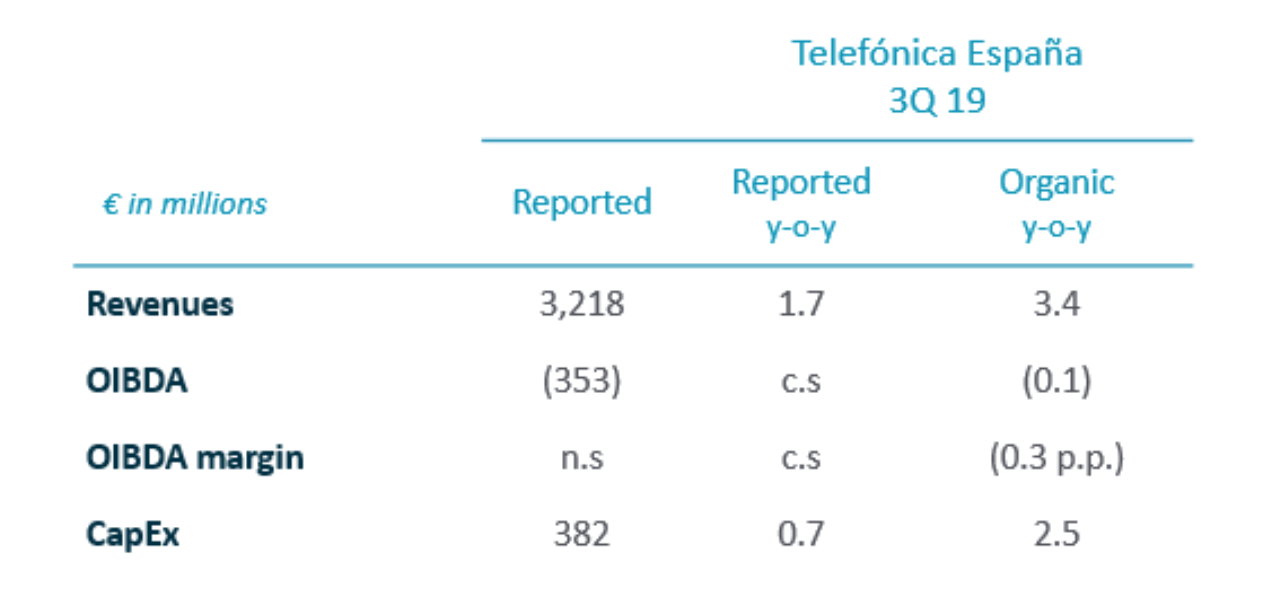

Telefónica España grew 1% in revenues thanks to a better convergent ARPU (+1.7% up to € 90,6): The pace of growth in service revenues accelerated in the third quarter to +1.0% y-o-y (+0.7 p.p. vs. Q2 19) and OIBDA grew again in organic terms (+0.1%, +1.8 p.p. vs. the previous quarter). This performance reflects the differential offer of Telefónica España, based on growing convergent revenues (on a larger base and higher ARPU), business revenues and wholesale and others. The higher quality of the customer base fostered convergent ARPU growth to 90.6 € in the quarter (+1.7% y-o-y).

Revenues in the quarter (3,218M€) accelerated their growth to 1.0% y-o-y (+0.7p.p. vs. Q2), thanks to the improved performance of service revenues (+1.0%; +0.7 p.p. sequentially). Revenues from handsets increased 0.3% y-o-y. Revenues grew in all segments compared to 3Q18. Operating expenses in July-September were impacted by the recognition of a provision of €1,732m in personnel expenses, mainly associated with the 2019 voluntary redundancy plan, and, in addition, with the headcount reskilling programme and the update of estimates from the previous plan. This new suspension plan will generate close to 210M€ of recurring direct savings from 2020 in addition to those already captured with previous plans.

OIBDA in July-September rose again in organic terms (+0.1%; -1.0% in January-September), 1.8 p.p. better than in the previous quarter. The organic OIBDA margin stood at 40.1% in the quarter (-0.3 p.p. y-o-y) and at 39.6% in the first nine months (-0.6 p.p. y-o-y).CapEx in January-September grew 3.9% y-o-y and OIBDA-CapEx in organic terms amounted to €2,566m.

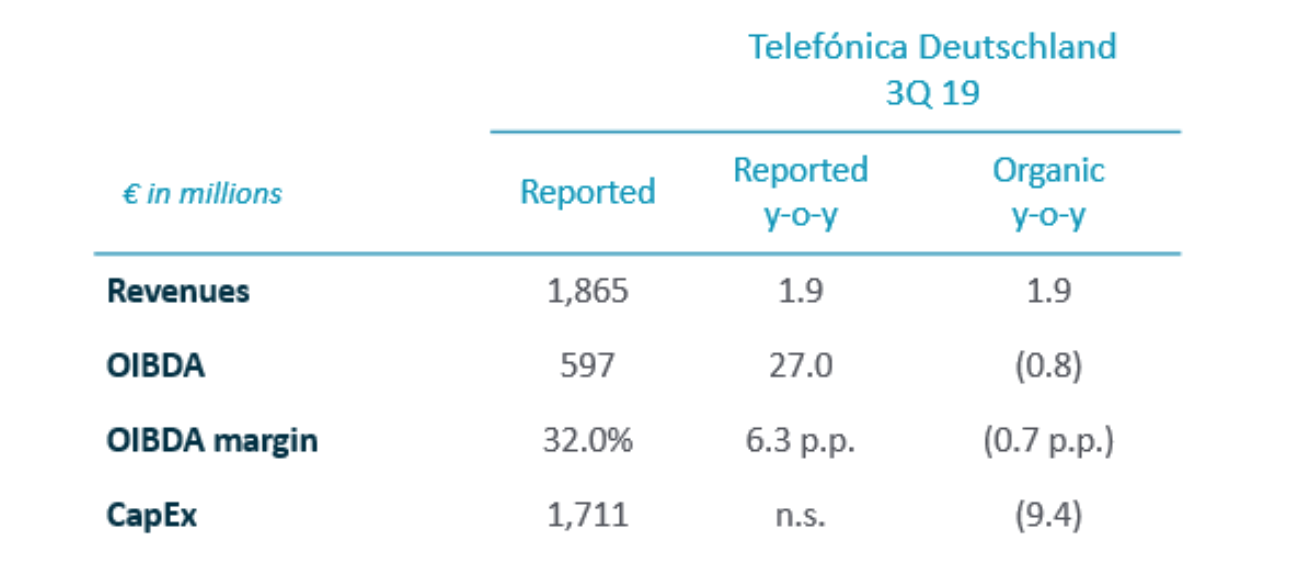

Telefónica Deutschland, solid operational evolution and good commercial momentum: Telefónica Deutschland achieved strong operational and revenue momentum in both, own and partner brands. The company continued improving its network quality through LTE roll-out, further enhancing customer experience. Contract churn remained at low levels. A “very good” rating of the My O2 app in the latest connect test also confirmed the improvement in customer experience.

Revenues amounted to €1,865m accelerating growth to +1.9% y-o-y in Q3 19 (€5,429m in 9M; +1.4% y-o-y). OIBDA of €597m in Q3 reduced its decline by 1.0 p.p. q-o-q to -0.8% y-o-y (€1,697m in 9M; -1.0% y-o-y). This improved trend was supported by top-line growth and remaining integration synergies (roll-over effects of €5m in Q3 and €35m in 9M) while also reflecting continued transformation & market investments into the O2 brand. IFRS 16 accounting changes accounted for a positive impact of €125m in Q3 (€362m in 9M). OIBDA margin stood at 32.0% in Q3 slowing its decline to -0.7 p.p. y-o-y (-0.6 p.p. in 9M).

CapEx of €2,207m in 9M included 5G spectrum obligations (€1,425m). The continued LTE roll-out with a focus on improving customer experience primarily drove the 5.7% y-o-y growth in 9M, easing front loaded H1 effects (+16.9% y-o-y in H1). OIBDA-CapEx amounted to -€509m for January-September 2019.

Telefónica UK, strong performance in main metrics: Telefónica UK continued posting a strong set of results in the third quarter, delivering healthy growth across all key financial metrics and all main segments of its customer base in a competitive market environment. The Company reiterated its market leading position and remained UK’s favourite mobile network with sector leading loyalty at 1.0%, supported by the continued success of its innovative propositions such as “Custom Plans”. Towards the end of the quarter and coinciding with the latest smartphone launches, Telefónica UK successfully introduced its first offer for customers seeking unlimited mobile data while providing upselling opportunities.

Revenues posted healthy growth of 4.1% y-o-y to €1,773m (€5,184m; +4.7% in 9M). OIBDA grew strongly by 5.7% y-o-y and reached €543m in Q3 19 (+6.2% in 9M; €1,595m), mainly driven by healthy top-line performance and supported by ongoing efficient cost management. OIBDA margin increased by 0.4 p.p. y-o-y in Q3 (+0.4 p.p. y-o-y in 9M).

CapEx amounted to €652m in 9M19, up 6.1% y-o-y, reflecting continued investment in network capacity, customer experience and the start of laying the foundations for 5G. OIBDA-CapEx grew by 6.2% y-o-y in 9M to €943m.

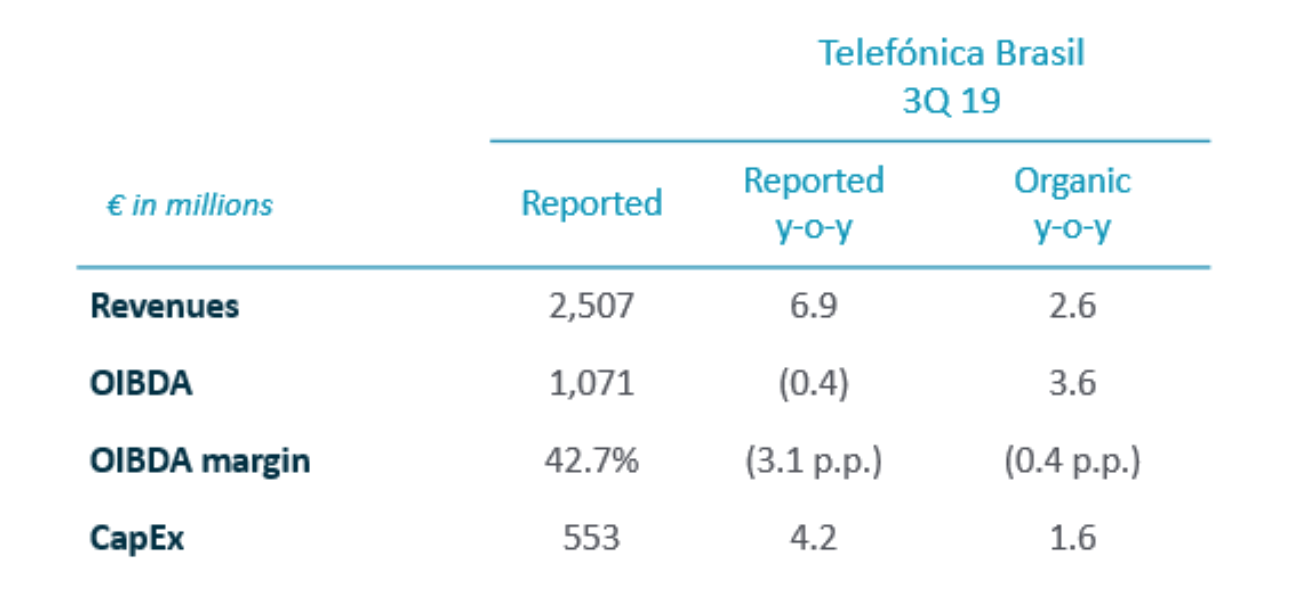

Telefónica Brasil obtains the highest growth in the last 15 quarters: Telefónica Brasil posted a significant revenue growth acceleration in Q3 to +2.6% y-o-y, the highest in the last 15 quarters, namely thanks to strong mobile service revenues (3 p.p. sequential improvement in contract and 6 p.p. in prepay).

Revenues in the quarter (€2,507m) accelerated their growth to +2.6% y-o-y (+1.6% in 9M) thanks to the improved performance of the mobile business and despite the decline in the fixed business and the regulatory impact. OIBDA reached €1,071m (+€109m due to IFRS 16 and +€324m in 9M) and returned to positive growth (+3.6% y-o-y; -0.6% in 2Q; +2.0% in 9M). OIBDA margin in the quarter stood at 42.7% (+0.4 p.p. y-o-y; 41.4% in January-September, +0.2 p.p. y-o-y).

CapEx in January-September amounted to €1,486m (+6.7% y-o-y), devoted to FTTH deployment (33 new cities deployed in the first nine months) and the expansion of the 4G network to 3,190 cities (88.5% population coverage; +1 p.p. y-o-y). CapEx accounted for 20% of revenues (+1 p.p. y-o-y). OIBDA-CapEx reached €1,635m in the first nine months, -2.9% as a result of the acceleration of investments.

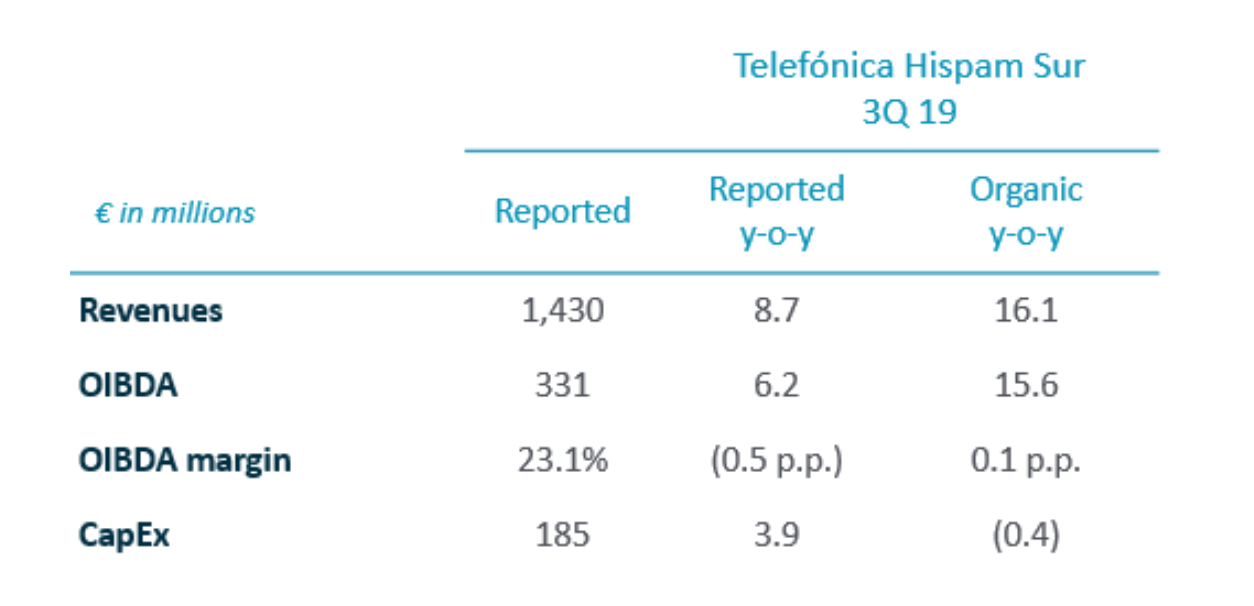

Telefónica Hispam Sur, solid y-o-y growth: Hispam Sur’s third quarter results maintained a solid y-o-y growth trend in both revenues and OIBDA, reflecting growth in value accesses (contract and FTTx/Cable), tariffs update in Argentina and savings from digitalisation.

Revenues amounted to €1,430m in Q3, up 16.1% y-o-y (+16.3% in 9M) mainly on growth in value, tariffs update in Argentina, back to growth in Peru after two and a half years, and acceleration of broadband revenues in Chile; all of this despite the regulatory impact in Chile and Peru (impact of -1.6 p.p. in the quarter’s growth, -1.8 p.p. in 9M). OIBDA (€331m in Q3; +€22m due to IFRS 16 and +€81m in 9M) grew 15.6% y-o-y in the quarter (+13.6% in 9M). OIBDA margin stood at 23.1% (stable y-o-y; 26.5% in January-September, -0.7 p.p. y-o-y).

CapEx for January-September amounted to €678m, +9.8% y-o-y mainly allocated to the deployment of LTE, FTTx and cable networks. CapEx represented 14% of revenues (-1 p.p. y-o-y). OIBDA-CapEx totalled €589m in 9M (+17.9% y-o-y).

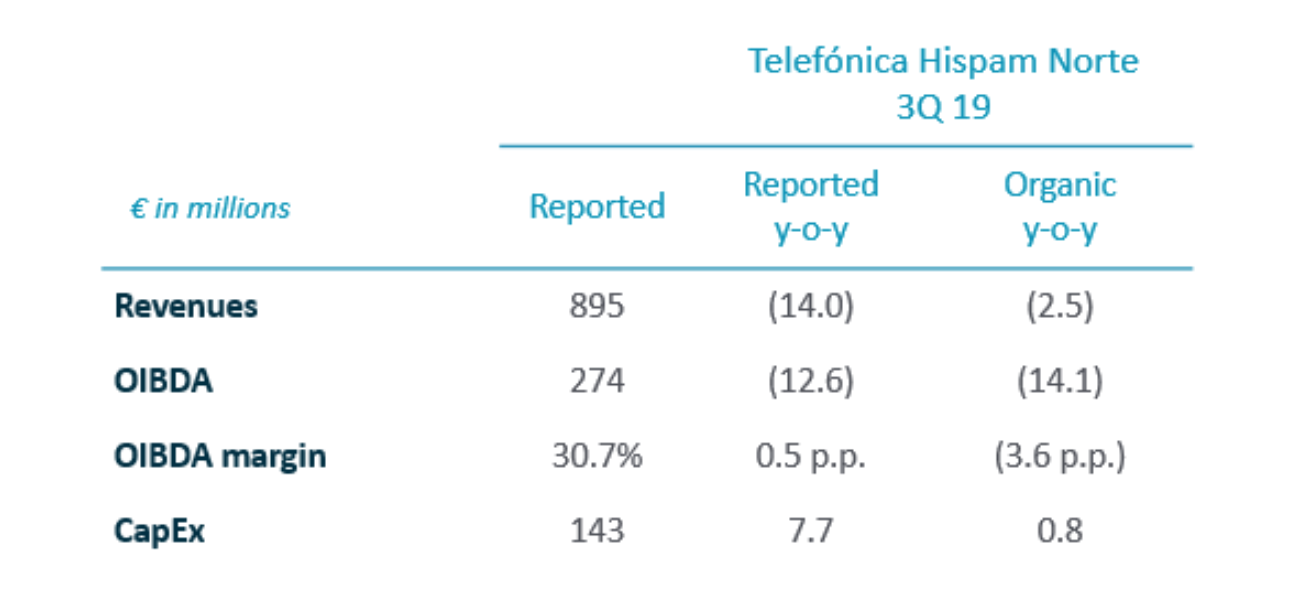

Telefónica Hispam Norte, high competitive intensity: Hispam Norte’s results showed similar trends to those seen in the previous quarter, and remained affected by the competitive intensity and by 2.5 GHz and 1,900 MHz spectrum commitments in Mexico, registered as OpEx instead of CapEx since Q4 18. Since 1st of September, and after the closing of its sale, Telefónica Panamá was no longer consolidated (Nicaragua since 1st of May and Guatemala since 1st of January), the closing of the divestments in El Salvador and Costa Rica are still pending.

Revenues (€895m) fell 2.5% y-o-y in the quarter (€2,880m, -0.4% in 9M), although the reversed trend in Mexico is particularly noteworthy (+0.6% y-o-y). OIBDA (€274m; +€37m following IFRS16 adoption; +€116m in 9M) decreased 14.1% y-o-y in the quarter (€799m in 9M, -14.0%). OIBDA margin stood at 30.7% (-3.6 p.p. y-o-y; 27.7% in 9M, -3.8 p.p.).

CapEx (€327m in January-September) rose 2.1% y-o-y. Furthermore, in the quarter €18m were registered for spectrum renewal in the 7.5 GHz and 23 GHz bands in Mexico. CapEx (excluding spectrum) represented 10% over sales in 9M (+0,2 p.p. y-o-y). OIBDA-CapEx totalled €472m in January-September.

Definitions:

Organic growth: Assumes average constant foreign exchange rates of 2018, except for Venezuela (2018 and 2019 results converted at the closing synthetic exchange rate for each period) and excludes the hyperinflation adjustment in Argentina. Considers a constant perimeter of consolidation. Excludes the effect of the accounting change to IFRS 16, write-downs, capital gains/losses from the sale of companies, restructuring costs and material non-recurring impacts. CapEx excludes spectrum investments.

Related documentation

PRESS RELEASE THIRD QUARTER RESULTS 2019

PRESS RELEASE THIRD QUARTER RESULTS 2019

PRESENTATION OF RESULTS FOR THE THIRD QUARTER OF 2019

INFOGRAPHICS RESULTS THIRD QUARTER 2019

Shareholders and Investors Section

QUARTERLY RESULTS

QUARTERLY RESULTS

Here you have data about the conference call, in which the most significant aspects of the results are commented.

Other news of interest

QUARTERLY RESULTS SECOND QUARTER 2019

QUARTERLY RESULTS SECOND QUARTER 2019

QUARTERLY RESULTS FIRST QUARTER 2019