The proposed EU Corporate Sustainability Reporting Directive (CSRD), published on 21 April 2021, marked a turning point with regard to what companies should report, how and with what guarantees.

The goal is to ensure that they publicly provide sufficient, adequate information about their risks and opportunities, as well as their impacts on people and the environment. In this context, the concept of double materiality has arisen.

The challenge for companies is to analyse and understand what is expected of them and respond appropriately

The Commission has acknowledged that in order to increase the quality of the information disclosed by companies it is necessary to ensure consistency in reporting. To this end, the European Financial Reporting Advisory Group (EFRAG) plans to publish five cross-cutting standards – which will cover information about matters that are key to the relationship between a company’s sustainability issues and its strategy, business model, governance and organisation – and six conceptual guidelines, so that regulators can ensure certain concepts are suitably translated.

Double materiality determination process

Guidelines for double materiality

In January, EFRAG published one of the batches of this set of guidelines on double materiality. It explained the meaning of impact materiality and financial materiality:

- Impact materiality: identifying material matters when the undertaking is connected to actual or potential significant impacts on people or the environment over the short, medium or long term, including both impacts directly caused by the undertaking and impacts which it has or may have in its entire value chain.

- Financial materiality: differing from the definition of materiality used in financial reporting, this refers to identifying material matters that trigger financial effects on undertakings, that is, that generate or may generate risks or opportunities that influence future cash flows and therefore the enterprise value in the short, medium or long term.

The goal is to determine which sustainability topics or sub-topics are relevant for the undertaking; therefore it is necessary to define appropriate information about them. A matter may be material from the impact perspective or from the financial perspective, or from both perspectives.

The proposal highlights several aspects in the process of determining material matters:

- The same importance is given to impact materiality as to financial materiality.

- The Board of Directors should identify relevant sustainability topics for the company before performing the materiality assessment.

- The (positive or negative) impact on all affected stakeholders and not only the needs of users as stakeholders must be taken into account in the undertaking’s information on sustainability.

The case of Telefónica

At Telefónica we started to work on this approach in 2021 as a determining element of our strategy and decision-making; we published our double materiality information in the 2021 Consolidated Management Report.

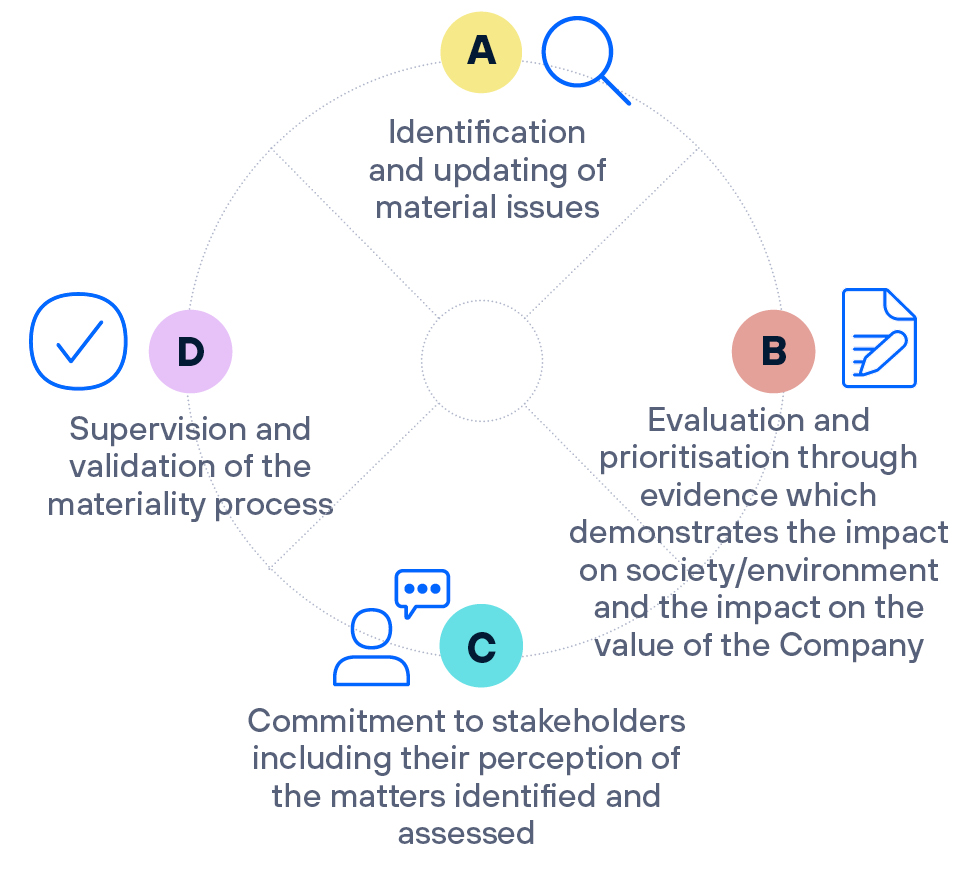

In the determination process, we followed four steps: identification and updating of material matters, evaluation and prioritisation from the impact perspective and the perspective of the Company’s value, inclusion of stakeholders’ perceptions, and internal and external validation and supervision of the results of the matrix.

Telefónica published its double materiality analysis for the first time in the 2021 Consolidated Management Report

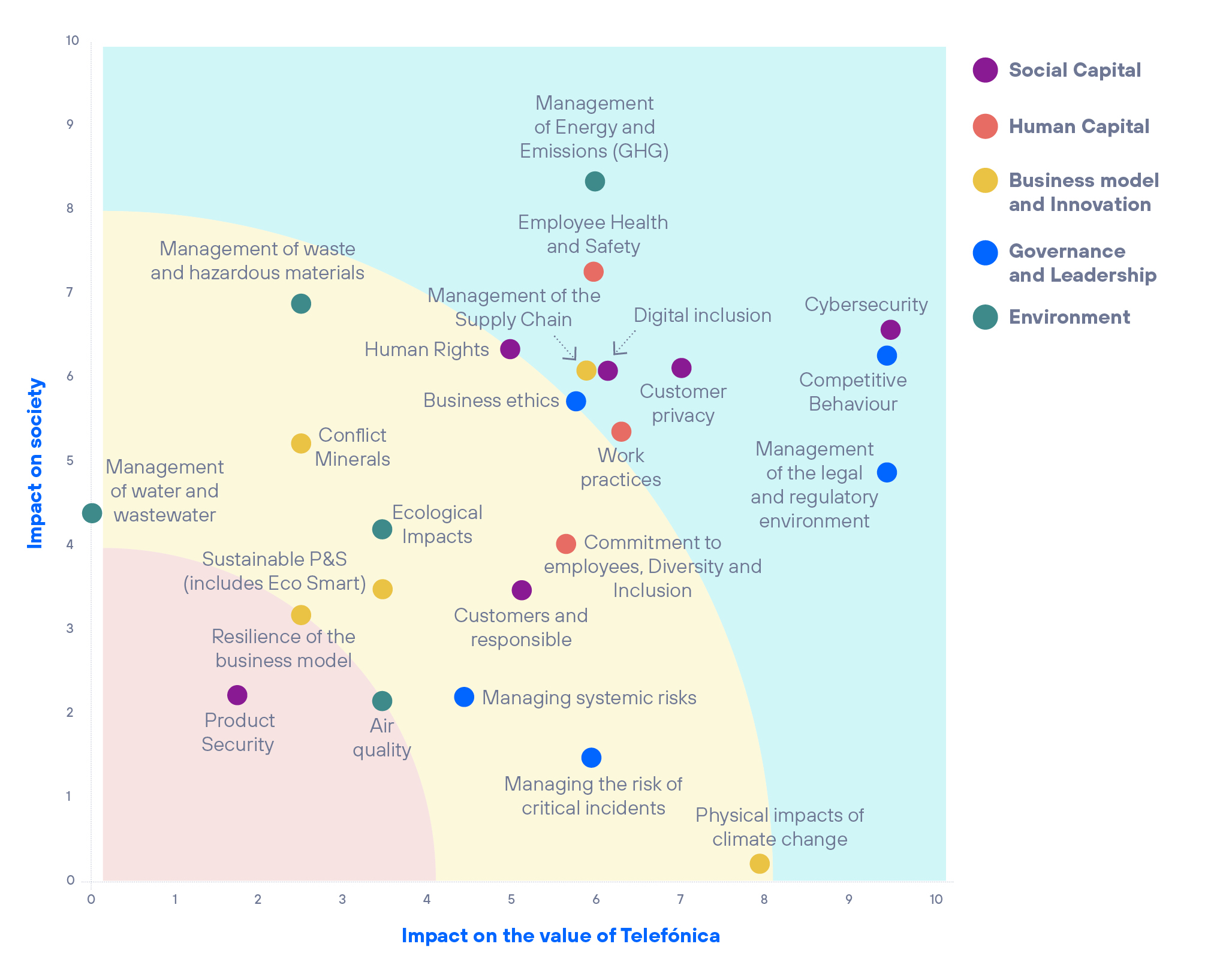

Reference to multiple external sources, participation by key areas to identify the Company’s risks and opportunities and the importance of key matters for the different stakeholders has resulted in an exhaustive and strategic objective matrix, which has enabled us to establish our ESG roadmap.

Thus, the most important issues due to their considerable impact on society and/or on the value of Telefónica are cybersecurity, competitive behaviour; the economic, political and regulatory environment; management of energy and emissions; employee health and safety; customer privacy; digital inclusion; supply chain management; work practices; and business ethics.

Their importance has led us to formulate new goals and action that have been set out in the Company’s Responsible Business Plan, prepared at a global level and which focus on the different operations, depending on their circumstances.

In summary, double materiality enriches companies’ vision, helping to define their strategy better, prevent short-sightedness and short-termism, and to consider all stakeholders in their activities. The impact of a company on society and its value constitute a two-way street which is of benefit to everyone.