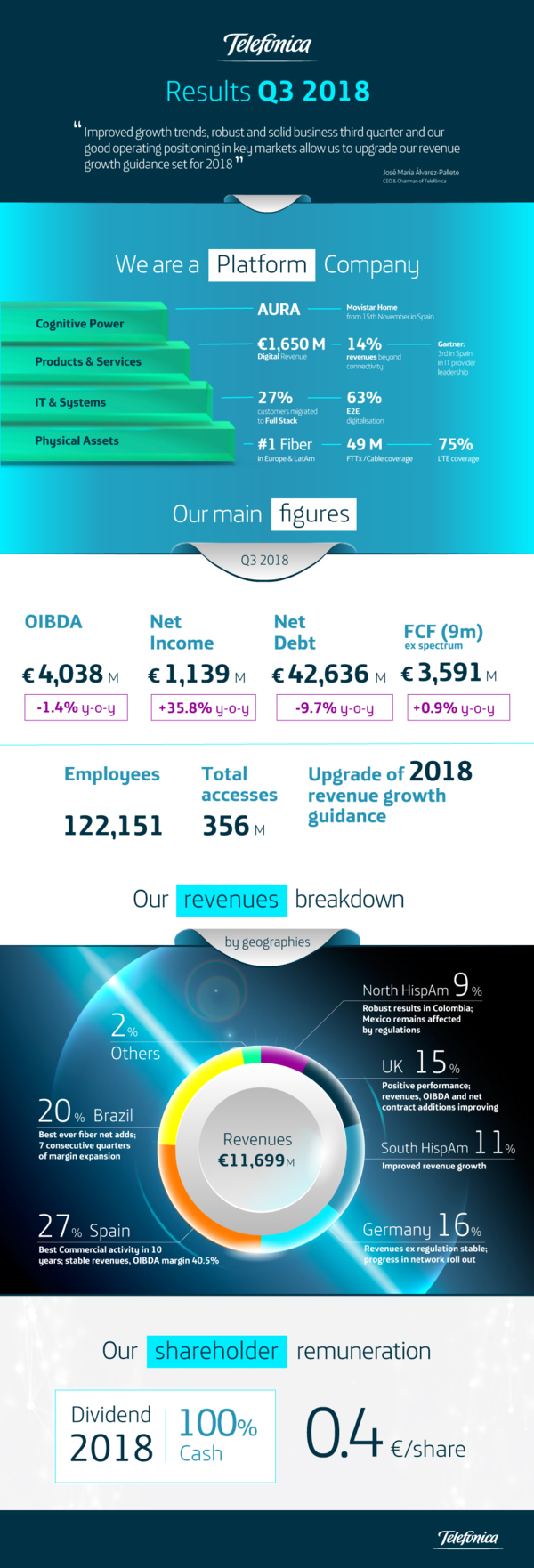

The Company upgrades its revenue growth guidance for 2018 to around 2%

Highlights:

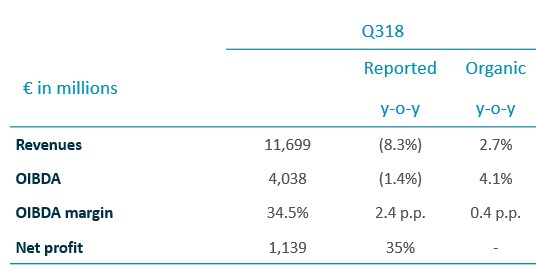

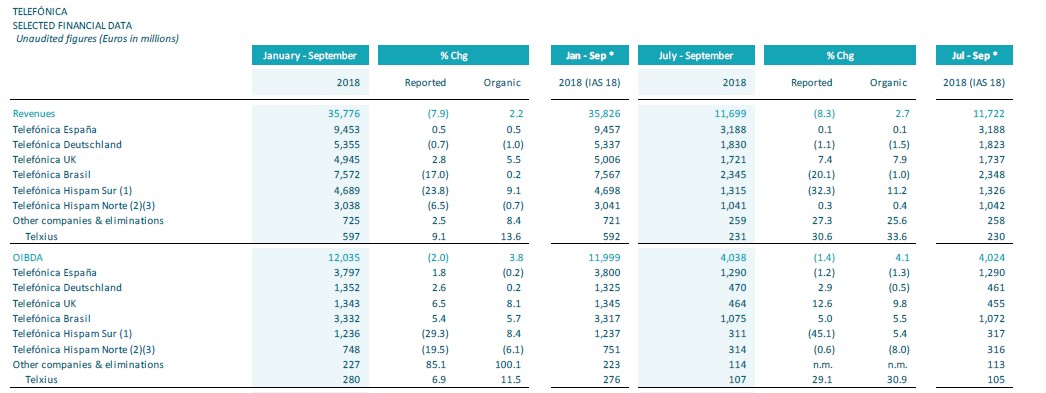

- Revenues for the period July-September reached €11,699m (-8.3% vs 3Q17) and accelerated their organic growth up to 2.7%, backed by the good evolution of service revenues (+1.2%) and the strong growth of handset sales (+20.7%).

- OIBDA registered €4,038m in the quarter (-1.4% vs 3Q17) and grew organically by 4,1%. OIBDA margin increased both in reported (2.4 p.p.) and organic terms (0,4 p.p.).

- Free cash flow grew 0,9% y-o-y in the first nine months, excluding spectrum payments.

- Net profit for the third quarter increased 35.8%, up to €1,139m.

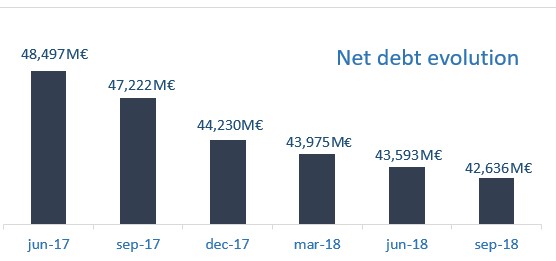

- Net debt reduced for the sixth consecutive quarter and stood at €42,636m at the end of September. This fall represents a reduction of nearly 10% year-on-year.

- Spain experienced the best commercial activity in a quarter in the last 10 years, and the UK increased its mobile service revenues for the 9th consecutive quarter.

José María Álvarez-Pallete, Executive Chairman of Telefónica:

“Third quarter results reflect the solid execution of our strategic priorities. To begin with, both high-value customers and their average revenue continued increasing, with a strong level of net additions in mobile contract (including the best figure for Spain over the last ten years), LTE, fibre and Pay TV. More and higher-value customers, coupled with stable churn rates, translates into higher business sustainability. If we add to that the wider coverage of our high-speed networks, the efficiencies we are already achieving in digitalisation and simplification, and the launch of Movistar Home via AURA, among others, we are further strengthening our future positioning.

Additionally, revenues and operating cash flow accelerated their organic annual growth, free cash flow reached 3 billion euros, up 0.9% versus the previous year excluding spectrum, and net debt decreased for the sixth straight quarter.

Improved growth trends, robust and solid business third quarter and our good operating positioning in key markets allow us to upgrade our revenue growth guidance set for 2018.”

Financial Results January-September 2018:

Telefónica today presented its results for the period January-September, which stand out for the high-value commercial activity during these months and for the improved growth trends, which allows the Company to upgrade its revenue growth guidance to around 2% (vs. around 1% previously), despite the negative impact from regulation (approximately 0.9 p.p.). It reiterates the OIBDA margin guidance (y-o-y expansion of around 0.5 p.p.), CapEx/Sales excluding spectrum (around 15%) and the dividend announced for 2018. Also relevant is the reduction in net debt (-9.7% vs 3Q17) and the financing activity of the first nine months of the year, close to €12,400m.

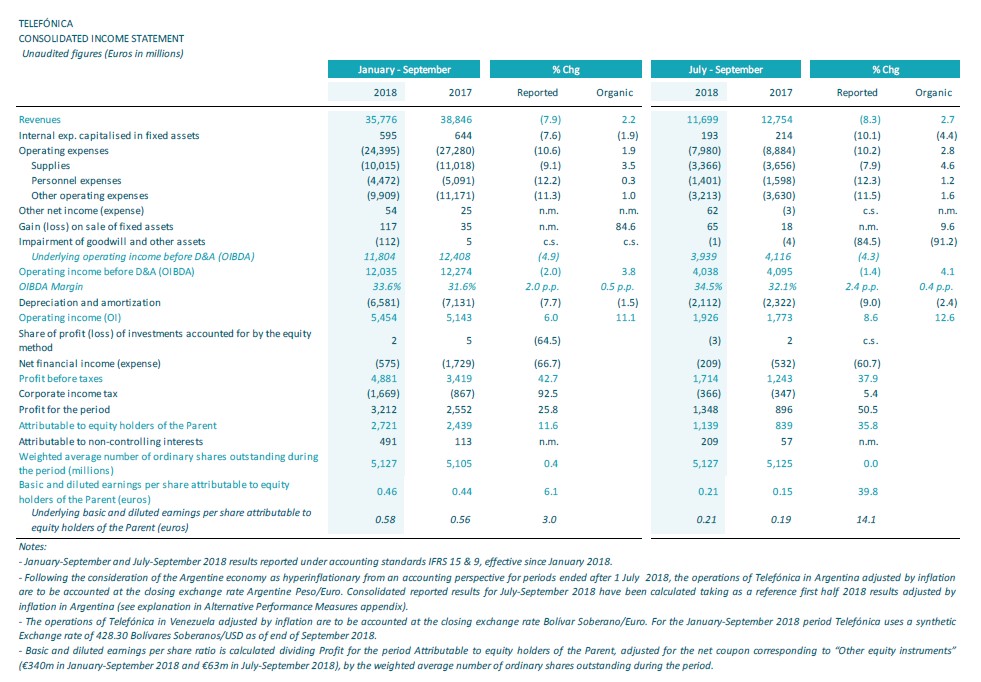

Revenues in the quarter stood at €11,699m (-8.3% vs 3Q17; €35,776m in January-September, (-7.9% vs 3Q17) and accelerated y-o-y growth to 2.7% in organic terms (+2.2% in January-September). They are based on improving mobile service revenues (+1.2% in the quarter; +0.9% in January-September) and the strong progress in handset sales (+20.7% in the third quarter; +19.0% in the nine months). Mobile data revenues increased in the quarter by 7.8% y-o-y in organic terms (+7.9% in January-September), and already represent 61% of mobile service revenues (+4 p.p. y-o-y in organic terms). Excluding the negative impact of regulation (-1.0 p.p. in the quarter and -1.1 p.p. in January-September), revenue growth would have accelerated to 3.7% y-o-y in organic terms in the quarter (+3.3% in the nine months).

Operating expenses totalled €7,980m in the quarter and decreased 10.2% y-o-y in reported terms (-10.6% in January-September 2018).

Operating income before depreciation and amortisation (OIBDA) totalled €4,038m in the third quarter, decreasing by 1.4% y-o-y. In January-September, OIBDA amounted to €12,035m (-2.0% y-o-y). In organic terms, OIBDA increased by 4.1% y-o-y in the quarter (+3.8% in January-September), reflecting the positive revenue evolution, savings from digitalisation and simplification, and cost containment efforts.

Excluding the impact from regulation (-1.3 p.p. in the third quarter and -1.9 p.p. in January-September), OIBDA would have risen by 5.4% y-o-y in organic terms in the quarter and 5.7% in the first nine months. OIBDA margin stood at 32.7% in the quarter in organic terms 34.5% (+0.4 p.p. y-o-y; 34.5% reported, +2.4 p.p. In January-September, it reached 32,5% organic (+0.5 p.p. y-o-y; 33.6% reported, +2.0 p.p. y-o-y).

In this regard, net profit in the third quarter reached €1,139m and grew 35.8% y-o-y (€2,721m in January-September; +11.6% y-o-y).

Moreover, the depreciation of foreign currencies against the euro, in particular the Brazilian real and Argentine peso, had a negative impact on the Company’s reported results. In the third quarter, the exchange rate evolution (excluding the hyperinflation adjustment) reduced y-o-y growth of revenues by 8.1 p.p. and OIBDA by 9.5 p.p. (-8.5 p.p. and -9.8 p.p. respectively in January-September). However, the negative impact of the depreciation of currencies at OIBDA level decreased significantly in terms of cash flow generation, since the depreciation also entailed lower payments in terms of CapEx, taxes, interests and dividends to minority shareholders.

Reported variations of the consolidated financial statements for January-September 2018 reflected the adoption of IFRS 15 and 9 since 1 January 2018 (results of January-September 2017 are reported following prior accounting standards). Organic variations excluded the impact of the accounting change to IFRS 15 in 2018 (-€23m in revenues and +€15m in OIBDA for the third quarter; -€50m and +€36m respectively in the first nine months). The accounting change to IFRS 9 had no significant impact on the results.

Additionally, the Group has applied hyperinflation accounting to its companies whose functional currency is the Argentine peso for periods ending 1 July 2018. The inflation adjustment on the financial statements is calculated retroactively since 1 January 2018, with a negative impact on the consolidated results of the Telefónica Group in July-September (-€361m in revenues, -€123m in OIBDA, -€112m in OI and -€76m in CapEx) and January-September (-€618m in revenues, -€229m in OIBDA, -€281m in OI and -€123m in CapEx).

Third quarter results have been affected by other factors. In terms of OIBDA, the impacts were as follows: a Brazilian court ruling (€307m), contingencies in Brazil (-€110m), hyperinflation adjustment in Argentina (-€123m), restructuring costs (-€34m), and capital gains on the sale of towers (€24m) and digital companies (€21m).

Debt reduction for the sixth consecutive quarter

CapEx in the first nine months of 2018 totalled €5,680m (+4.7% y-o-y) and included €612m in spectrum payments. In organic terms, it increased by 5.0% and continued to focus on the radical transformation of networks deployment of ultra broadband networks and network virtualisation) and quality improvement. Operating cash flow (OIBDA-CapEx) reached €6,354m in January-September 2018 and increased by 0.7% y-o-y. In organic terms, it grew by 2.9% reflecting the good business performance. Free cash flow reached €2,957m in the first nine months of the year (-8.3% y-o-y) and increased by 0.9% excluding spectrum payments.

Net financial debt at September (€42,636m) decreased for the sixth consecutive quarter, up to €1,594m compared to December 2017, from which €957M were reduced in the third quarter. Year-on-year it decreased 9.7%.

During the first nine months of 2018, the financing activity of Telefónica increased to approximately €12,360m equivalent (without considering the refinancing of commercial paper) and focused on maintaining a solid liquidity position, and refinancing and extending debt maturities (in an environment of low interest rates). Therefore, as of the end of September, the Group has covered debt maturities for the next two years. The average debt life stood at 9.16 years (versus 8.08 years in December 2017).

Intense commercial activity in high value customers

In a context where connectivity and digitalisation are key to the global digital ecosystem, Telefónica continued developing its platforms and offering a differential customer experience. Telefónica Group’s access base stood at 356.3m at the end of the September, virtually stable y-o-y, after a quarter with a strong commercial momentum both in customer acquisition and quality. This commercial activity in high-value customers accelerated average revenue per access to 3.5% y-o-y in organic terms (+3.0% in January-September), while churn remained stable.

The growth in high value accesses was driven by the strong demand for data, speed and content: i) LTE customers totalled 111.5m (+25% y-o-y); ii) mobile contract accesses (121.6m; +7% y-o-y); iii) “smartphones” (+7% y-o-y; 166.8m); iv) FTTx/Cable (12.8m; +21% y-o-y) represents 59% of total fixed broadband accesses (+10 p.p. y-o-y), with a coverage of 49.0m premises passed with proprietary network (+15% y-o-y); and v) pay TV (8.8m; +6% y-o-y).

The Group’s FTTx/Cable coverage reached 81.0m premises passed at the end of September (49.0m for proprietary network), 20.8m FTTH in Spain, 9.0m FTTx/Cable in Hispam (+45% y-o-y) and 19.3m in Brazil. LTE coverage stood at 75% at September (+6 p.p. y-o-y; 92% in Europe and 69% in Latam) and LTE traffic represented 64% of the total traffic. In parallel, progress has been made towards 5G with the use of Massive MIMO and 4.5G deployment in Germany, Brazil, Mexico and Colombia.

The weight of revenues from services beyond connectivity continued increasing and account for 14% of the Group revenues (+1 p.p. vs. September 2017). Digital service revenues account for €1,630m in Q3; +19.5% y-o-y and €4,901m in 9M; +25.3%. As an example, 63% of processes are digitalised and managed in real time (+8 p.p. y-o-y), improving “time-to-market” and customer experience. Also, digital channel sales (28% of total) increased by 50% y-o-y in overall accesses and by 73% in Fusión.

Definitions:

Organic growth: Assumes average constant foreign exchange rates of 2017, except for Venezuela (2017 and 2018 results converted at the closing synthetic exchange rate for each period) and excludes in 2018 the hyperinflation adjustment in Argentina. Considers constant perimeter of consolidation. Excludes the effects of the accounting change to IFRS 15 in 2018, write-downs, capital gains/losses from the sale of companies, tower sales, restructuring costs and material non-recurring impacts. CapEx excludes spectrum investments.

Results by geographies:

(y-o-y changes in organic terms)

Telefónica España. Telefónica España posted an excellent commercial activity in the third quarter of 2018, with record figures in fixed and mobile portability, the highest mobile contract net additions in ten years and the highest fixed broadband net additions since “Fusión” was launched. This intense commercial activity is primarily related to high-value customers as a result of our differential value offer in the start of the football season under a new competitive scenario.

In financial terms, revenues and OpCF maintained its y-o-y variation stable and the OIBDA margin surpassed the 40% despite of the bold commercial effort, higher content costs in the quarter, regulatory impact and the loss of the wholesale contract with Yoigo/Pepephone.

Quarterly revenues reached €3,188m (+0.1% y-o-y) thanks to the stability of service revenues (€3,090m; +1.4% when excluding the impacts of MTR cut and MVNO loss commented before, in line with the previous quarter) and higher handset sales (+4.6% y-o-y vs. +7.5% in Q2). In the first nine months of the year, total revenues (€9,453m) and service revenues (€9,176m) grew by 0.5% and 0.3% y-o-y respectively.

OIBDA in July-September rose to €1,290m and the OIBDA margin stood at 40.5%, -0.6 p.p. year-on-year, mainly because of the greater growth in net content cost. OIBDA reached €3,797m in the first nine months (similar to the same period in 2017) and the OIBDA margin remained virtually stable y-o-y (-0.2 p.p. excluding capital gains).

CapEx in the first nine months of 2018 totalled €1,157m (+4.8% y-o-y), affected by execution calendars. The operating cash flow stood at €2,641m (-1.9% y-o-y, excluding capital gains).

Telefónica Deutschland. Telefónica Deutschland maintained strong operational momentum in the third quarter of 2018 as the updated 02 Free tariff portfolio with Boost & Connect continues to be well received by customers, further fuelling data growth and supporting ARPU-up strategy. For the first nine months of the year, results were fully on-track with full year guidance, supported by successful synergy capture and a clear value over volume approach.

Revenues totalled €1,830m declining by -1.5% y-o-y (€5,355m in 9M 18; -1.0% y-o-y) and -0.8% y-o-y excluding regulatory effects in Q3 18. OIBDA (€470m in Q3 18) decreased by -0.5% y-o-y (€1,352m in 9M 18; +0.2%) due to lower incremental synergies (~€10m in Q3 18; ~€75m in 9M 18, mainly rollover effects of the FTE restructuring and incremental savings from network consolidation), while regulatory effects stood at -€17m (-€48m in 9M 18). Mobile service revenues reached €1,339m declining by 0.9% y-o-y (3,937m in 9M 18; -0.8% y-o-y) mainly due to negative regulatory effects (mainly RLAH) and due to less support from visitor roaming. MSR ex-regulation remained stable y-o-y in Q3 18 (+0.2% y-o-y in 9M 18). However, OIBDA margin was 25.7% in the quarter and expanded by 0.3 p.p. (25.2% in 9M 18; +0.3p.p.) supported by value over volume marketing approach and focus on efficient cost spending.

CapEx amounted to €740m in the first nine months and increased by 7.6% y-o-y as a result of entering the final stage of network consolidation; project is fully on-track to be completed by YE18. At the same time, LTE rollout is pushing ahead. Incremental CapEx synergies of ~€35m in January-September 2018 were mainly related to LTE network rollout. As such, operating cash flow (OIBDA-CapEx) was down -7.2% y-o-y to €612m in January-September 2018.

Telefónica UK. Telefónica UK delivered another strong set of results, again growing key metrics in the third quarter of 2018. The Company remains the UK’s favourite mobile network carrier with a total base of 32.3m customers, while O2 continues to lead market loyalty with the lowest churn. At the end of August, the Company launched an industry-first proposition, “Custom Plans”, providing customers with flexibility and choice allowing them to customise their plans by choosing contract terms (up to 36 months), amount of upfront payment and data plan, supporting its customer led, mobile first strategy. The Company continues to invest in its award winning network with rapid deployment of the spectrum awarded in the recent auction.

Revenues continued to increase to €1,721m, up 7.9% y-o-y (€4,945m up 5.5% y-o-y in the first nine months). This revenue increase was mainly driven by higher value smartphone sales supported by the launch of “Custom plans”, as well as the inflation (RPI) effect on airtime rates in April. OIBDA totalled €464m in the quarter, representing an accelerated growth of +9.9% y-o-y (€1,343m up 8.1% in the first nine months), mainly as a result of the strong top-line performance and also supported by a reduction in Annual Licence Fee payments, a commercial settlement of €18m, and a reduced impact of roaming (RLAH-Roam Like At Home) in the quarter. Excluding this commercial settlement OIBDA would registered an increase of 5.3% y-o-y. Thus, OIBDA margin improved by 0.5 p.p. y-o-y to 26.9% in Q3 18 (27.2%; +0.6 p.p. in the first nine months).

CapEx amounted to €1,202m was up 3.0% y-o-y when compared with January-September 2017, on the back of the ongoing investment in network capacity and customer experience. Operating cash flow (OIBDA-CapEx) strongly improved by 12.8% y-o-y to €141m in January-September.

Telefónica Brasil. In the third quarter of 2018, Telefonica Brasil continued showing a solid commercial performance, especially in value, which, together with the gradual reduction in costs (digitalisation and simplification), enabled to increase OIBDA margin for the seventh straight quarter (+2.3 p.p. y-o-y) and to post a solid y-o-y growth in OIBDA (+5.5% in organic terms in the quarter). The drop in fixed voice revenues and the uncertain macroeconomic environment were factors behind the slowdown in revenues.

Revenues in the quarter (€2,345; €7,572m in 9M) decreased by 1.0% y-o-y (+0.2% in 9M), affected by the deterioration of the macroeconomic environment and regulatory impact (excluding this regulatory impact, revenues would have increased 0.5% in Q3 and +1.8% in 9M). OIBDA reported in the quarter was positively impacted by €307m from the court decision related to the exclusion of the state tax on goods and services (ICMS) from the PIS/COFIN tax base (Programa de Integração Social/Contribuição para Financiamento da Seguridade Social) in Vivo between July 2004 and June 2013 (in addition to the €485m recorded in the second quarter associated with the equivalent court decisions for the subsidiaries Telesp and TData from September 2003 to July 2014) as well as to diverse contingencies amounting to -€110m (-€216m in 9M). Therefore, OIBDA reached €1,075m (€3,332m in 9M) and increased in the quarter in organic terms (excluding the aforementioned impacts, IFRS 15 and exchange rates) by 5.5% (+5.7% y-o-y in 9M in organic terms). The OIBDA margin increased by 2.3 p.p. y-o-y to 37.2% in organic terms (36.6% in 9M; +1.9 p.p. y-o-y).

CapEx in the first nine months stood at €1,422m (+14.0% y-o-y) and was mainly allocated to expanding the fibre and 4G networks and improving quality. Operating cash flow stood at €1,910m in the first nine months decreasing by 1.9% y-o-y.

Telefónica Hispam Sur. During the third quarter, Hispam Sur maintained solid growth in revenues and OIBDA, despite the highly competitive environment, especially in Peru. It is worth noting the growth in value, with positive net additions in contract for the fourth consecutive quarter and sustained increase in FTTH accesses.

Revenues in Q3 rose to €1,315m and increased by 11.2% y-o-y (+9.1% in 9M) driven by the aforementioned good operating performance and the tariffs updates. Operating expenses increased by 13.6%, accelerating versus the previous quarter (+9.7% in 9M) on higher expenses in Argentina (inflation impact on salaries update, customer service and higher energy costs). Personnel expenses include €24m of employee restructuring costs in the quarter (€4m in Argentina and €20m in Peru). OIBDA reached €311m in Q3 (+5.4% y-o-y). Quarterly OIBDA margin stood at 23.7% (-1.5 p.p. y-o-y) and at 26.4% in January-September (-0.2 p.p. y-o-y).

CapEx totalled €685m (+10.8% vs. 9M 17) and operating cash flow (OIBDA-CapEx) amounted to €551m (+5.7%).

Telefónica Hispam Norte. Hispam Norte delivered a solid commercial performance in the third quarter of the year, with positive net additions in the most valuable accesses (mobile contract, fixed broadband and pay TV), which allowed operational revenues to reverse its y-o-y trend and grow 0.4% y-o-y to €1,041m (-0.7%, €3,038m in 9M) led mostly by the performance improvement in Colombia. Excluding negative regulatory impacts, revenues would have increased 2.3% y-o-y (+1.3% in 9M). Operating expenses totalled €773m in the last three months (+4.4% y-o-y; €2,305m, +2.5 % in 9M) mainly reflecting higher network expenses through the region, which were partially offset by the reduction in commercial expenses and efficiency measures. OIBDA amounted to €314m in the quarter (-8.0% y-o-y; €748m, -6.1% in 9M), negatively affected by regulation in Mexico. Excluding this impact, OIBDA would have remained virtually stable y-o-y (-0.6%; + 1.8% in 9M) mostly due to the acceleration in revenue growth in Colombia. OIBDA margin stood at 30.2% (-2.6 p.p. y-o-y; 24.6%, -1.5 p.p. in 9M).

CapEx totalled €297m in 9M (-30.5% y-o-y) and was mainly allocated to the expansion of fixed and mobile infrastructures. Operating cash flow (OIBDA-CapEx) rose to €451m and increased 16.8% when compared to 9M 17.