The Climate challenge

“There’s one issue that will define the contours of this century more dramatically than any other, and that is the urgent threat of a changing climate”.

That is how the former President of the United States, Barack Obama, referred to the Climate challenge ahead of us. Not only we are facing a paramount threat, but we must do so against the clock given the closing window to reduce GHG emissions and reverse global warming.

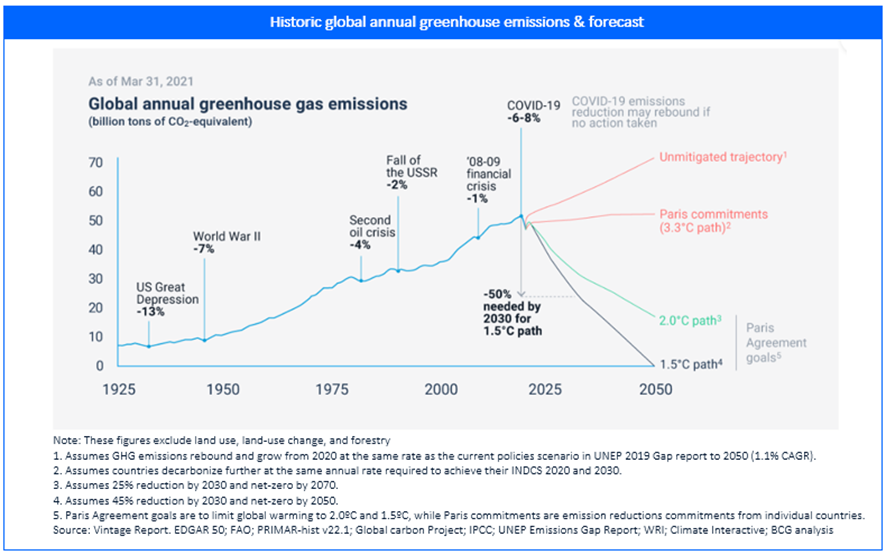

According to the latest assessment released by the Intergovernmental Panel on Climate Change (IPCC), Human activities, mainly through GHG emissions, have led the global surface temperature to reach 1.1ºC above pre-industrial levels in just 150 years and the current path indicates it could reach well over 3.5ºC by 2090. To give some context, during the last ice-age global temperatures were just 6ºC lower than today so it is not difficult to guess what a rise of +3ºC could entail for our planet.

Unprecedented Challenges call for unprecedented Measures

The good news about this is that Humanity have been facing challenges of similar size across centuries and, united by purpose and a unique desire to evolve (and survive), have successfully found ways to tackle most of them.

Governments, institutions, corporates and investors, mainly driven by a greater societal shift towards climate awareness and conscious behaviors, have acknowledged the size and urgency of the challenge, carrying out important developments in the last few years:

- +130 countries representing 88% of the global GHG emissions have now set Net Zero Targets up to 2060.

- Comprehensive and more demanding regulation has been arising, spearheaded by the CSRD and the EU Taxonomy in Europe, and followed by international standards like SASB and the ISSB, proposed by the International Finance Reporting Standard (IFRS).

- Over +5.000 companies, including 1/3rd of the world’s largest publicly-traded corporates, have now set and are actively tracking its climate pledges under standards like SBTi.

- +34% of the assets managed by European Fund Managers are already framed within Article 8 & 9 funds, meaning they include ESG criteria and even minimum commitments for sustainable investments into their thesis.

But… is it enough?

According to BloombergNEF, global low-carbon energy transition investments in 2022 amounted to $1.1T, reaching an historic milestone and surpassing annual fossil fuel investment for the first time in history. However, the last assessment from the IPCC says we are not on track to keep the 1.5ºC objective needed to reverse global warming within reach. Recent developments are definitely not enough and the world needs to get serious about climate action now.

What is needed?

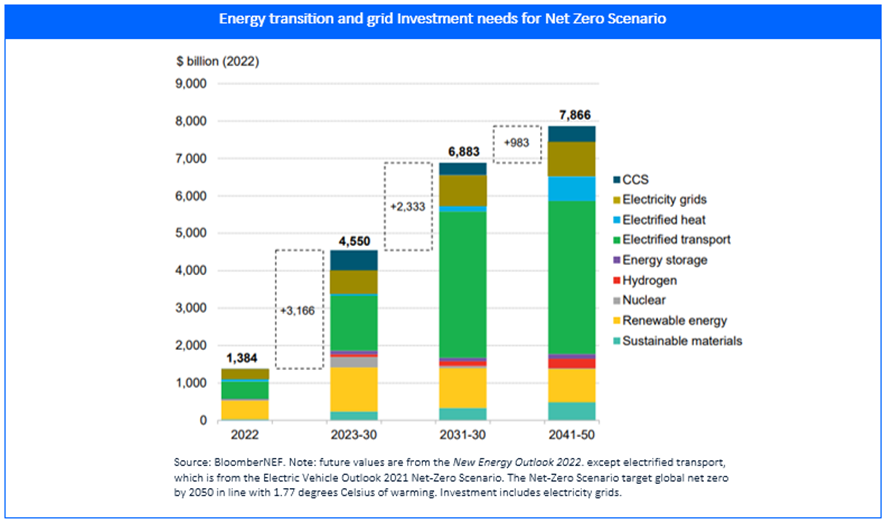

In its New Energy Outlook, BloombergNEF forecasts that annual global investment on low-carbon energy transition and smart grids should average $4.5T along the next decade in order to get on track for Net Zero, meaning annual investment should triple from the current level.

While Electrified Transport, Renewable Energy and Grids will drive the lion’s share of investment (over 72% of total estimated investment), Carbon Capture, Removal and Storage will be one of the fastest growing areas, demanding +$500B by 2030.

Given the current investment split, which is 50-50% Public-Private and expected to remain like that in the short-term, we can foresee huge designated budgets and capital inflows into the greater sustainability framework, with some relevant examples like:

- $1T committed over the next decade from the US via the IRA and the EU via the European Green Deal.

- Several multi-billion Climate Funds launched by Corporate investors like Amazon ($2B) & Microsoft ($1B) and fund managers like TPG ($7B).

Taking a closer look into the Venture Capital Ecosystem

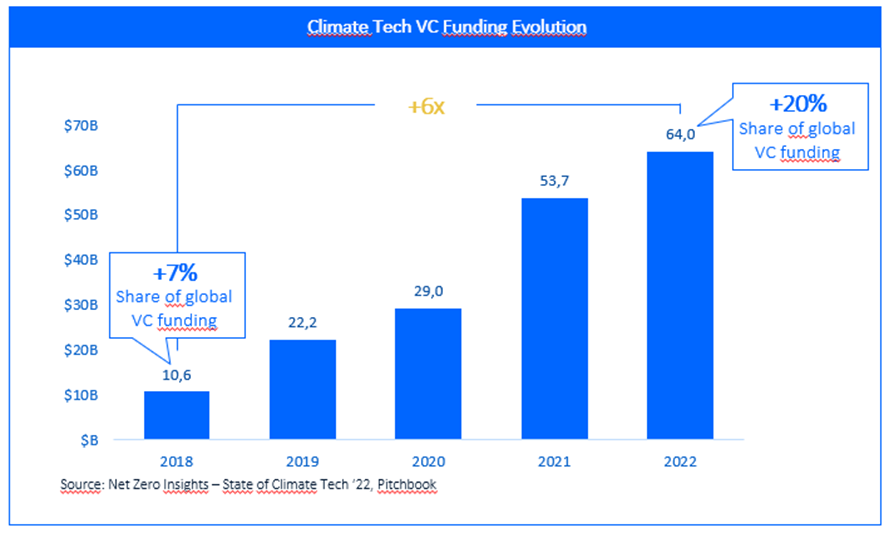

Deep diving into our perimeter of expertise, the Venture Capital ecosystem, activity has been booming in the Climate Tech field with 6x growth in the last 5 years.

Despite the broader market correction seen along the past year, +$60B were poured into Climate Tech during 2022. This amount represents over a fifth of the total VC funding, having grown from 7% to +20% in the last 5 years. Unsurprisingly, Corporate VCs are leading the effort, participating in +35% of the total funding share with relevant examples like Amazon, Microsoft, Google, BP or GM launching their own vehicles and being among the most active investors in the field.

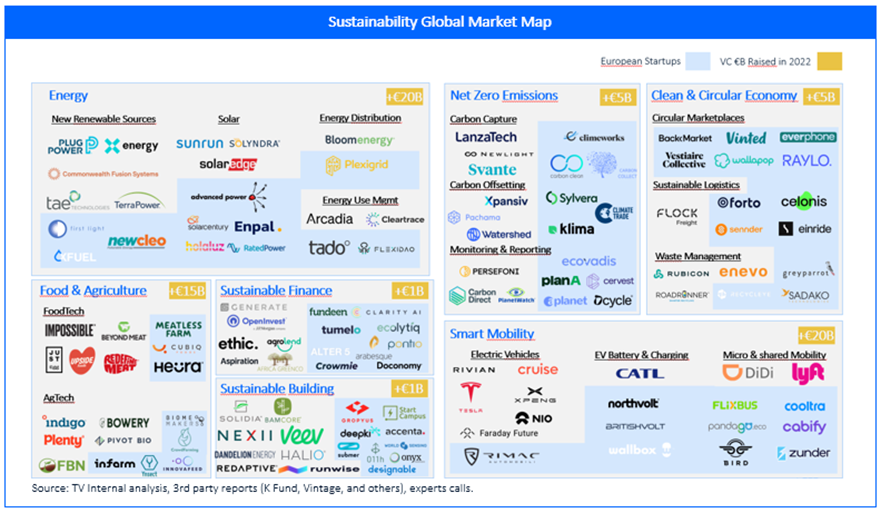

Looking at the most relevant segments within the sustainability field, Energy & Smart Mobility drive the lion’s share of investment with +$20B raised by startups of each field just the last year. Meanwhile, Startups in the Carbon Capture, Use and Storage and in the Circular Economy sectors are rapidly gaining traction, having raised +$5B each.

Furthermore, this trend is not expected to shy away anytime soon given the increasing fundraising activity and the huge dry powder ready to be deployed into climate startups. Having raised +$90B by new private Climate Investment Funds in the last 2 years, there is an estimated $37B of dry powder available for VC in the short-term.

Sustainability at the Core of Telefónica Strategy

Telefónica Ventures is the Corporate Venture Capital of Telefónica Group and as such, we aim to tackle the great challenges facing the Telco industry to create new businesses and verticals aligned with the core strategy of the group. With AuM of +€155M, 15 companies in portfolio and positions in +10 VC funds around the globe, we have helped boost +€400M of joint business between Telefónica and our portfolio companies.

In that regard, Telefónica has long acknowledged the importance and urgency of the Climate & Social challenges, integrating ESG vision as a key pillar into the current Corporate Strategy plan. This commitment has been verified and recognized by several industry-leading analysts & rankings such as the CDP Climate A List (for 9 consecutive years), FTSE4Good and S&P Dow Jones Sustainability Index Europe, among others.

In order to understand the rationale behind Telefónica’s strong commitment towards the climate challenge it is important to highlight the “Double Materiality” concept. Apart from the obvious risks that the global warming poses for the world and its urgency, it also presents relevant operating, financing and revenue-driving opportunities that can add great value for Telefónica’s business in the long term.

For the sake of this post, we will focus on the “Environment” pillar of the ESG strategy. Here, Telefónica has identified three main priorities with the objective of “building a greener future”:

- Climate goals. Through the use of renewable energy sources, a more energy-efficient approach and offsetting the non-avoidable emissions, the Group is on track to become Net Zero by 2040. This commitment made Telefónica the first company in the Telco sector to receive SBTi validation for its net zero targets.

- Circular Economy Goals. By integrating circular economy principles into our processes and within our supply chain, the Group plans to become a Zero-Waste company by 2030 while improving ROCE along the way.

- Supporting our customers to decarbonize their activity through our digital products and services. By offering Cloud, IoT, Big Data and Digital Home solutions our customers have already avoided +81.7M tCO2e. Our clients need to promote and invest in digitalization, we see new business opportunities to help them achieve their green targets.

Our view on the future of Climate Tech

Given the growing ecosystem of energy & climate-related startups we see everyday, we strongly believe that Telefónica Ventures should help the group and our customers achieve its ESG goals by partnering with founders tackling some of the most pressing challenges of our days.

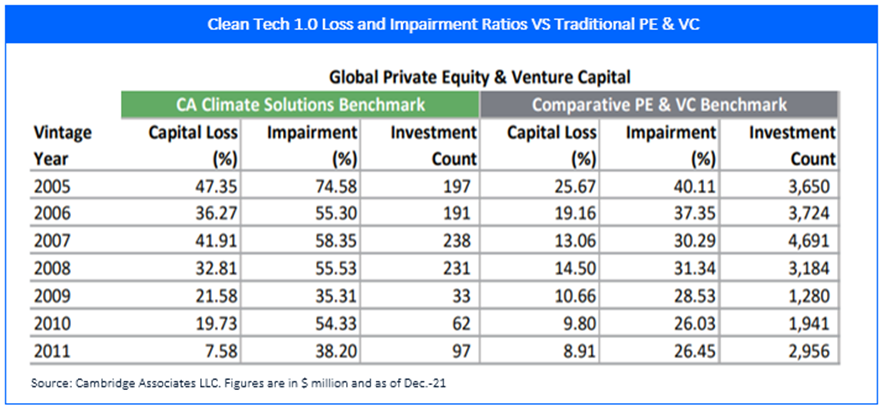

However, the VC play in sustainability is still to be proven after the first “failed” wave of Climate Tech back in the early 2000’s, where Cambridge Associates estimates that investors lost nearly half of the capital invested as seen below.

Looking at the big picture, three main barriers led the first wave to fail:

- Technical risk. Experimental technologies usually undergo a period of unsustainable unit economics and expensive overheads that must be subsidized until commercially-ready.

- Capital intensity. This subsidized period is intensified if the technologies are asset-heavy and results in large capital needs for which VCs were not ready.

- Product-market fit. Given the nascent stage of the clean economy, the markets failed to develop fast enough for the wave of technologies and business models to scale and fit in the exit timings and paths of the VC cycle.

With most of these barriers (almost) broken down a decade later, we believe Climate Tech has an exciting future ahead, both for humanity and for the ones riding the next wave:

- Technological advancements from the last wave have led to +90% cost reduction in some of the asset-heavy technologies like wind and solar.

- The increasing urgency of the challenge has aligned governments and regulation will be a critical booster for clean markets to establish and scale faster.

- The previous reasons along with some other developments have led governments, corporates, investors and even consumers to put skin in the game, ensuring capital availability for climate founders throughout the whole cycle.

Investment Thesis

Based on our thoughts above and trying to tackle the main goals set by Telefónica, we are looking to back and partner with businesses developing cutting-edge solutions primarily (but not limited to) the following sectors:

- Net-Zero Emissions. Digital platforms helping corporates to manage the increasingly complex world of carbon management.

- ESG accounting & reporting software helping corporates to comply with increasing disclosure regulations.

- Solutions targeting supply chain & Scope 3 emissions, which usually account for +70% of the total carbon footprint.

- API-based carbon offsetting platforms ensuring transparency and high-quality credits.

- Traceability and certification frameworks & technologies tackling the greenwashing issue and providing reliable benchmarks and guidance.

- Energy Consumption & Efficiency. Digitalplatforms providing tools to measure, optimize and reduce energy consumption.

- Energy use management & optimization plaftorms helping customers fight the rising energy prices and the increasing mix of energy sources.

- 24/7 renewable energy traceability software to shift from annual to daily and hourly-based renewable energy certifications.

- Energy-efficient computing solutions to tackle the unsustainable energy power needs of rising AI models like LLMs, spatial computing systems, etc…

- Clean & Circular economy. Phygital models helping companies introduce circularity within their supply chains, eliminating discretionary waste while improving ROCE.

- Electronics refurbishment circular models targeting both B2B and B2C customers.

- Product Lifecycle Analysis platforms (PLAs)tracking climate risks and footprint along the supply chain.

- Sustainable logistics solutions helping digitize the industry and reduce unnecessary waste and emissions.

- Any other digital solutions providing emissions reduction, energy efficiency or waste reduction services like smart metering solutions, earth observation platforms…

Bibliography

- The energy transition: A region-by-region agenda for near-term action | McKinsey

- The Three Challenges of a Sustainability Transformation | BCG

- Investing in Climate-Tech, Why We Think This Time Is Different – Vintage Investment Partners (vintage-ip.com)

- Climate tech: enabling technologies and the Spanish startup scene — K Fund

- State-of-Climate-Tech-22-Net-Zero-Insights.pdf

- New dry powder for a new climate (ctvc.co)

- COP27: What have global leaders done on climate change in 2022? – BBC News

- Which countries have set a net-zero emissions target? (ourworldindata.org)

- Net Zero Tracker | Welcome

- Los fondos Artículo 8 y Artículo 9 más grandes del mercado – FundsPeople España

- AR6 Synthesis Report: Climate Change 2023 — IPCC

- Net Zero Stocktake 2023 | Net Zero Tracker