Telefónica is a wonderful company with great opportunities ahead. The Company has very strong and hard to replicate assets and capabilities

Strengths

- Four strong core markets with strong operations. We lead in two of our core markets.

- Spain: Fifth telco market in Europe, with highly developed convergence and network infrastructure.

- Brazil: Largest market in LatAm, with high growth and three national mobile players.

- Germany: Largest telco market in Europe with untapped opportunity in fibre.

- UK: Second telco market in Europe, and largest B2B Digital Services market.

- Experts in network operations with robust, advanced infrastructure.

- Pioneers in convergence strategy.

- Highly talented and professional team.

- Deep know-how in most areas.

- Strong culture: pride and sense of belonging.

Transform & Grow is the plan Telefónica needs to capture the opportunities ahead, improve financial flexibility and generate sustainable value for all shareholders.

As an additional upside to the Plan, we will pursue in-market Telco consolidation to unlock profitable scale and enable value-accretive investments.

Six strategic pillars to become a ‘best-in-class European Telco’, with profitable scale.

- Deliver best-in-class customer experience

- Expand B2C offering

- Scale B2B

- Evolve technological capabilities

- Simplify Telefónica’s operating model

- Develop talent

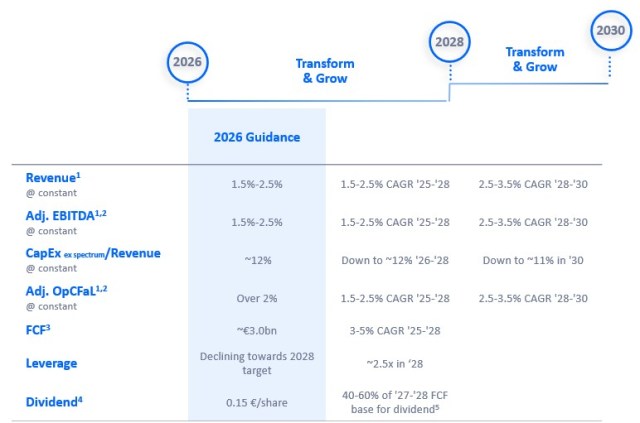

Guidance anchored on specific levers across 6 pillars.

1. Constant: assumes constant FX (average FX 2025), constant perimeter and excludes the contribution to growth from Venezuela

2. Adjusted figures consider constant perimeter and derived capital gains/losses and do not include restructuring costs, write-offs and material non-recurring impacts

3. FCF for Guidance includes reported FCF from continuing operations and excludes non-recurring spectrum payments, employee commitments and VMO2 dividends

4. Dividend payable in cash in June of the following year.

5. FCF base for dividend = FCF base for guidance – Employee commitments + VMO2 dividends.

Financial strategy based on a disciplined capital allocation. Clear financial priorities to create long-term value.

- De-risked and growing FCF

- Anchored investment grade a must, deleveraging

- Sustainable remuneration linked to FCF

- Improved financial flexibility

- + Value accretive M&A

- Core markets opportunities

- Synergistic

- Financial disciplined